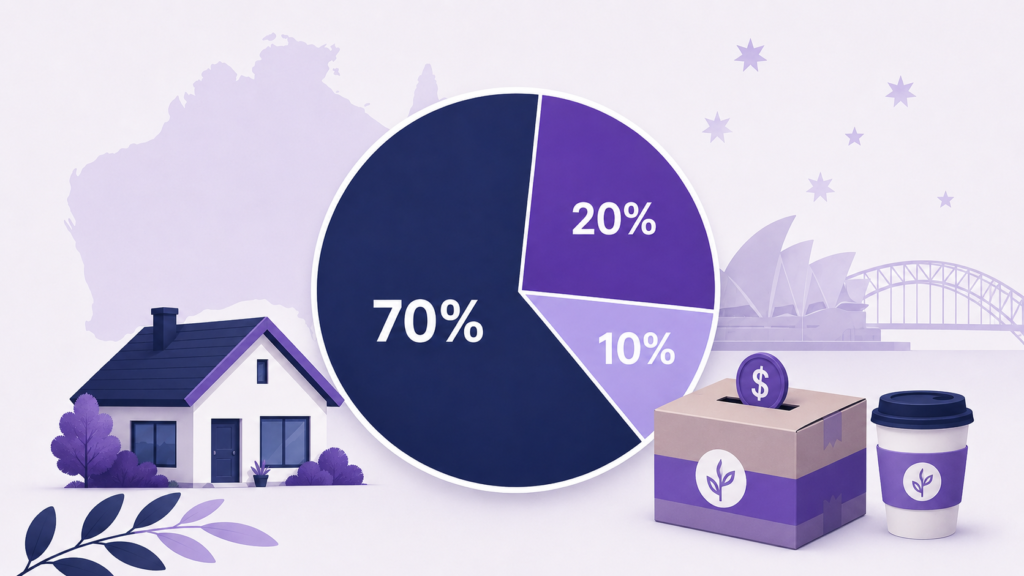

So you’ve probly heard the buzz about budget rules online. The 70/20/10 rule is one of the easier ones to follow. It splits your take-home pay into three simple buckets. Needs, savings, and a bit of fun.

What is the 70 20 10 rule money in plain English? You spend 70% on living costs. You save or pay debt with 20%. The last 10% goes to wants. It’s like dividing a pizza into three uneven slices. The biggest slice handles bills. Smaller ones cover the rest. No spreadsheets full of categories. No tracking every coffee. Bit refreshing, right?

In Sydney, where rent eats half your pay, simple matters. Same goes for Parramatta, Blacktown, or anywhere else with a high cost of living. This guide breaks it down for real Aussie life. Whether you’re moving across town or planning a long-haul move, money rules matter. Let’s get into the proper detail now.

How the 70/20/10 Budget Rule Works?

The 70/20/10 budget rule slices your after-tax income into three parts. Each part has one job. No overlap. No confusion. You start with your net income. Not gross. The amount that actually lands in your bank. Then you split.

It works because the math is dead easy. Anyone with a calculator and a pay slip can run the numbers.

70% Living Expenses (Needs)

Seventy percent covers your needs. Rent, groceries, fuel, electricity, internet, transport. The stuff you can’t skip without your life falling apart. This bucket is the heavy one. It’s where most of your pay disappears. In Sydney, this slice fills up fast.

What counts as a need? Anything that keeps you housed, fed, and able to work. Mortgage repayments, council rates, basic phone bills. Childcare too, if you’ve got little ones.

What doesn’t count? Streaming services, takeaway coffees, weekend brunch. Those go in the fun bucket. We’ll get there.

20% Savings & Debt (Future)

Twenty percent feeds your future self. This is where the 70/20/10 savings rule lives. You either stash this cash or knock down debt with it.

Got a credit card balance? Pay it down here. Got a car loan? Same bucket. No high-interest debt? Send it straight to savings. Smart move is splitting this bucket too. Maybe ten percent to debt, ten percent to savings. The 20 percent savings rule then becomes a hybrid plan.

This is also your moving fund. If you’re saving up for a removalist sydney to wollongong run, cash builds here. How much savings before moving out? At least three months of rent plus a moving budget.

10% Wants/Fun/ (Lifestyle)

Ten percent is your fun money. Movies, eating out, hobbies, weekend trips. This bucket is small but mighty.

How much fun money per month does that look like? On a $5,000 take-home pay, you’ve got $500 to play with. Not bad at all.

This slice keeps you sane. Skip it and you’ll bail on your budget by month two. Trust me on that one. Treats matter.

Why the 70/20/10 Budget Rule Works?

Simple rules stick. That’s the whole reason the 70/20/10 budget rule keeps gaining fans. You don’t need a finance degree to follow it. It also matches reality in expensive cities. In Sydney, rent alone can chew through 40-50% of net pay. Add bills and food, and 70% feels right.

The 50/30/20 rule assumes you only spend half on needs. Cute idea. Not realistic for most Aussies. The 70/20/10 plan respects the real cost of living. Plus, it works whether you earn $50k or $150k. The percentages flex. Only the dollar amounts change. You scale it up or down without breaking the rule.

It builds saving habits without burning you out. Twenty percent is a solid chunk. But it’s not so high you feel deprived all month.

Benefits of the 70/20/10 Budget Rule

There’s a few reasons this rule has fans across Australia. Let’s run through them quick.

Ideal for High Cost of Living

If you live in Sydney, Melbourne, or Brisbane, your rent is brutal. The 70/20/10 budget rule was made for places like these. It accepts that you’ll spend big on basics. Other rules pretend rent should be smaller. They don’t survive contact with reality in NSW. This one does.

It works for renters in Parramatta, owners in the Eastern Suburbs, and families in Blacktown. The math doesn’t care about postcodes. Just income and expenses.

More Flexible Than 50/30/20

The 50/30/20 rule splits things differently. Half on needs, 30% on wants, 20% on savings. Sounds nice. But who actually spends only half on needs in Sydney? Which budgeting method is best depends on your income and city. For high cost of living areas, 70/20/10 wins. For lower cost regions, 50/30/20 might fit.

Flex is the name of the game. The 70/20/10 rule lets needs run higher. It admits that rent is just expensive. No shame in that.

How to Use the 70/20/10 Budget Rule in Real Life?

Theory is one thing. Doing it is another. Here’s how to actually run this rule day to day.

Budgeting with Buckets

Three bank accounts. That’s the trick. One for needs, one for savings/debt, one for fun. Some people call this three-bucket budgeting. Pay lands in your main account. Then you transfer 20% to savings and 10% to fun. The remaining 70% covers bills. Done.

Visual buckets work because you stop mixing money. Your fun cash isn’t sitting next to rent money, tempting you. Out of sight, out of spend.

Automating Finance

Set up auto-transfers on payday. Pay hits, money moves. You don’t get a chance to spend it first. Most banks let you schedule these for free. Set it once, forget it. The 70/20/10 budget rule runs on autopilot.

Some folks also automate bill payments. That keeps the 70% bucket from getting skipped. Bills get paid first, then everything else falls in line.

Adjusting for Circumstances

Life isn’t a spreadsheet. Sometimes the rule needs to bend. New baby? Needs go up. Job loss? Everything changes overnight. Big moves shift the math too. If you’re hiring removalists or planning a Sydney to Brisbane removalists run, costs spike. Adjust the rule for that month.

The point is, don’t ditch the system because of one weird month. Tweak it. Come back to baseline next month.

How to Bucket Your Money Using the 70/20/10 Rule?

Bucketing is what makes the rule actually work. Without buckets, money mixes up. Mixed money gets spent on the wrong stuff. Here’s a real-world setup. Say your take-home is $6,000 a month. Bucket one gets $4,200. Bucket two gets $1,200. Bucket three gets $600.

You can use bank accounts, envelopes, or apps. A 70/20/10 budget spreadsheet works too. Whatever you’ll actually use day to day. I’d recommend digital for most people. Cash envelopes feel old-school cool. But they don’t fit modern life unless you really love physical money.

Apps like Up, ING Direct, and Pocketbook let you create sub-accounts. Each one becomes a bucket. Name them clearly so you don’t mix them up.

How to Calculate Your Spending for a 70/20/10 Budget?

Math time. Don’t worry, it’s quick.

Step one: find your net monthly income. That’s your pay after tax, super, and anything else taken out. The amount in your bank.

Step two: multiply by 0.70 for needs, 0.20 for savings/debt, 0.10 for fun. Or use percentages on a calculator.

Example. Net pay of $5,500.

- Needs: $3,850

- Savings/debt: $1,100

- Fun: $550

If your needs come in higher than $3,850, you’ve got a problem. Either income is too low. Or expenses are too high. The rule shows you where the gap sits.

What percentage of income should I save? With this rule, it’s 20%. But if you’ve got debt, half of that 20% might go to repayments. The 70/20/10 savings rule still applies. The split between debt and savings just shifts.

How much should I have left after bills? About 30% of your net pay total. That covers savings and fun together. If you’ve got less than that, time to look at expenses.

Different Versions of the 70/20/10 Budget Rule

People remix this rule all the time. Different versions fit different lives. Here are the common ones.

70% Needs, 20% Debt, 10% Savings

This version flips savings and debt. If you’ve got high credit card balances, debt comes first. The 20% goes hard at debts every month.

How to save money while paying debt? You don’t, not much. You let the 10% trickle into savings while you crush the debt. Once debt clears, you swap them back. This version fits people drowning in interest. Pay down what’s costing you 20%. Don’t earn 4% on savings while paying 20% on cards. That math loses every time.

70% Needs, 20% Savings, 10% Wants

Standard version. This is the classic 70/20/10 budget rule. Works for people without major debt issues. Most personal finance writers default to this split. It’s the cleanest one for normal life. Bills, future, fun. Three slots.

This version builds wealth steadily. Twenty percent into savings or super each month adds up fast. A decade of that, and you’re sitting pretty.

70/10/10/10 Method

This version splits the 30% three ways. Ten percent to savings, ten to debt, ten to fun. More balance, less focus. Some prefer this if their debt is medium-sized. You don’t ignore savings while paying off cards. You don’t ignore debt while saving. Both move forward.

The downside is slower progress on each goal. But mental wins matter too. Watching all three move feels good.

Other Names for the 70/20/10 Budget Rule

People call this rule different things. Same idea, different labels. Don’t get confused if you see these online.

70-20-10 Budgeting Rules

Some folks write it with dashes. 70-20-10 budgeting rules means the same thing as 70/20/10. The slashes or dashes don’t change the math. You’ll see this on forums, blogs, and money apps. Some prefer dashes because they’re easier to type. No deeper meaning to it.

70-20-10 Percentage Budget

This version emphasizes the percentages. Same rule, but the name reminds you it’s all about ratios. The 70-20-10 percentage budget is just a clearer name. Some readers like names that explain themselves. This one does.

Percentage-Based Budgeting

Broader term. Percentage-based budgeting includes 70/20/10, 50/30/20, and any other ratio rule. It just means you use percentages, not dollar amounts.

Why does this matter? Because percentages scale. You don’t need to redo your budget when you get a pay rise. Same rule, bigger numbers.

Three-Bucket Budgeting

The visual name. Three buckets, three jobs. Easy to picture, easy to remember. This name helps beginners. Telling a mate about three-bucket budgeting is less intimidating than throwing percentages around. The picture sticks.

Pros and Cons of the 70/20/10 Budget Rule

Like any rule, this one has trade-offs. Let’s be real about both sides.

Pros:

- Easy to set up, even for beginners

- Works for high cost of living areas like Sydney

- Doesn’t require tracking every dollar

- Builds savings habits without burnout

- Adapts to different income levels

- Simple to teach and explain

Cons:

- Might not save enough for FIRE goals

- Doesn’t handle irregular incomes well

- Can blur the line between needs and wants

- Doesn’t account for big one-off costs

- Some people need stricter tracking

- 10% fun bucket might feel tight

Truth is, no budget rule is perfect. It’s a starting point, not a religion. Use what works, ditch what doesn’t.

Does the 70/20/10 Budget Rule Work in Sydney?

Now for the local question. Sydney is its own beast when it comes to costs. Does this rule survive Harbour City prices?

Short answer: yes, but barely. Long answer: keep reading.

Sydney rent pressure

Sydney rent in 2026 is rough. A one-bedder in inner suburbs runs $600 a week or more. That’s around $2,600 a month before any other bills. For someone earning $6,500 net, that’s already 40% gone. Add bills, food, and transport, and you hit 70% before fun money. The rule barely fits.

In Parramatta, rents are slightly lower but still hefty. Same goes for Liverpool, Penrith, and the Hills District. Sydney rent pressure is real and constant.

Net income first

Always work from net income, not gross. Your gross pay isn’t your spending power. Tax, super, and HECS all come out first. If you earn $90,000 gross, your net might be $5,800 a month. Run the rule on $5,800. Not $7,500. That’s the trap.

People who use gross numbers always feel broke. Because they’re trying to spend money they never had.

When 70% fails

Sometimes 70% just isn’t enough for needs. Family of four in Sydney? Needs might hit 80% or more. Single parent with childcare? Even higher. When the rule fails, change the rule. Try 80/15/5 instead. Or move to a cheaper suburb. Or boost income with side work.

Don’t beat yourself up if the rule doesn’t fit. It’s a tool, not a rulebook from heaven. Adjust until your numbers add up.

Smarter local tweaks

Sydney has tricks that help. Off-peak rents in winter. Free events on weekends. Markets cheaper than supermarkets. Use public transport instead of running a car. That alone can save $300+ a month. Transport is one of the biggest needs after rent.

For movers, off-peak weeks save cash too. The cheapest month to move sydney isn’t December. It’s usually winter, mid-month, mid-week.

Who the 70/20/10 Budget Rule Works Best For?

This rule isn’t for everyone. Let’s look at who gets the most out of it. It suits people who hate complicated tracking. If you’ve tried fancy apps and given up, this might stick. Three buckets, three jobs, done.

It works for renters in expensive cities. Especially anyone in Sydney, Brisbane, or Melbourne. The 70% needs slot fits real costs. It’s good for people with steady incomes. Salary workers especially. Self-employed folks with bumpy pay might need a different approach.

Young professionals starting out love it. So do families learning to budget together. Parents teaching teens about money find it easy to explain. People moving home benefit too. Moving costs hit hard. The 20% bucket builds your moving fund. Whether you’re hiring movers parramatta crews or planning a longer move, the savings stack up.

Tips for Success With the 70/20/10 Budget Rule

A few tips to make this rule actually work for you. From people who’ve done it.

Start with net income. Always. Don’t fall for gross-pay traps.

Automate everything you can. Manual transfers fail. Auto ones don’t.

Review monthly, not weekly. Budgets shift over time. A monthly check beats daily stress.

Keep your fun bucket separate. Mixed money gets spent wrong.

Use a moving house budget template if you’re relocating. Big life changes need their own plan. Move costs can blow the rule for a month.

Be honest about needs vs wants. Netflix isn’t a need. Neither is fancy coffee. Be brave with that line.

Build an emergency fund first. Three months of expenses, then start splitting normally. Without a buffer, every emergency wrecks your plan.

Track your progress quarterly. Are you saving more than last quarter? Are debts smaller? That’s the real test.

Talk to your partner. Joint budgets fail when one person hides spending. Have the awkward chat.

Adjust for life changes. Marriage, kids, moves, job changes all shift the rule. Don’t pretend nothing changed.

She’ll be apples if you stick with it for a few months.

Better Budget Rules to Compare With 70/20/10

The 70/20/10 isn’t the only game in town. Other rules exist. Some might fit better. Let’s compare.

50/30/20 rule

The famous one. 50% needs, 30% wants, 20% savings. Cleaner split, but tougher in expensive cities. Works great in regional areas where rent is lower. Falls apart in Sydney for most people. The 30% wants slot is generous. Maybe too generous.

Use this if you live in a cheaper city. Or if you’ve got a high income that gives you room to flex.

Zero-based budgeting

Every dollar gets a job. Down to the last cent. Sounds intense because it is. You list every expense, every saving goal, every category. Then assign your full income across them. Nothing left over.

Great for control freaks (no shade). Brutal for people who want simple. The 70/20/10 budget rule is way easier than zero-based.

60/20/20 option

Tighter on needs, equal on wants and savings. 60% needs, 20% wants, 20% savings. Works for higher earners or low-cost regions. If you can keep needs at 60%, this rule gives more room for fun. And the same savings rate as 70/20/10.

Some retirees use this version. They have lower needs (no mortgage, kids gone) and more flex.

Custom split methods

Make your own rule. Some people use 65/25/10. Others 75/15/10. Or even 40/40/20 for high savers. Custom splits fit unique lives. Just keep three categories, three percentages. Make sure they add to 100%.

The rule is yours. The math just has to work.

Not Sure if the 70/20/10 Budget Rule Is Right for You?

Still on the fence? That’s fair. Let’s talk about who should skip it.

If you’ve got irregular income, this rule struggles. Freelancers, gig workers, commission salespeople. Your income jumps around. Fixed percentages feel weird. If you’re in serious debt, you need a debt-focused plan. Maybe the avalanche or snowball method first. Come back to 70/20/10 after debts clear. If you love detailed tracking, you’ll hate this. It’s too loose. Try YNAB or zero-based instead. If you live really cheaply, this rule wastes savings. Could you save 30%? Maybe 40%? Don’t let a rule cap your potential.

But for most Aussies, especially in big cities, it works. Especially if you’re new to budgeting. Or new to having a regular job.

How budgeting connects to moving

Big moves are budget killers. Moving home shifts your budget like a quake shifts the ground. The 20% bucket is where moving funds grow. Whether you book Sydney to Melbourne removalists or a cross-city run with cheap removalist sydney teams, the math shows up. The cost doesn’t care about your feelings.

How much do removalists charge per hour matters when you plan. Same goes for the hourly rate for removalists across Australia. In Sydney, it’s around $130 to $180 per hour for two movers and a truck.

In Parramatta, similar rates apply. In rural areas like with removalists dubbo or dubbo removalists, prices vary. Smaller crews cost less. Bigger jobs cost more. If you’re moving, get quotes early. Use a moving house budget template. Add it to your savings goal. That’s the rule in action.

Sydney’s diverse moving needs

Sydney is full of new arrivals. Many search in their own language first. Dutch speakers type “verhuizen” before they ever search “removalists.” French speakers type “demenagement” the same way. Migrant families especially feel the pinch. Moving away from family adds emotional cost on top of financial cost. The rule helps you plan, even when feelings get messy.

Got kids? Timing matters. The worst age to change schools sits between 11 and 14. The worst age to change schools australia data backs this up too. The worst age to move a child is when they’re settled in deep friendships.

The best age to move a child is under seven or after high school. Their roots aren’t as deep yet. Pick your moment if you can. When a family moved last year in our records, the savings bucket made it possible. Without it, they’d have run dry by week three. Budget first, move second.

Real Costs to Add to Your Budget Bucket

Here’s what to expect when you plan a move. Real numbers help. Vague hopes don’t.

Local moves with movers near me. $130 to $180 per hour for two crew. Most jobs run 3 to 6 hours.

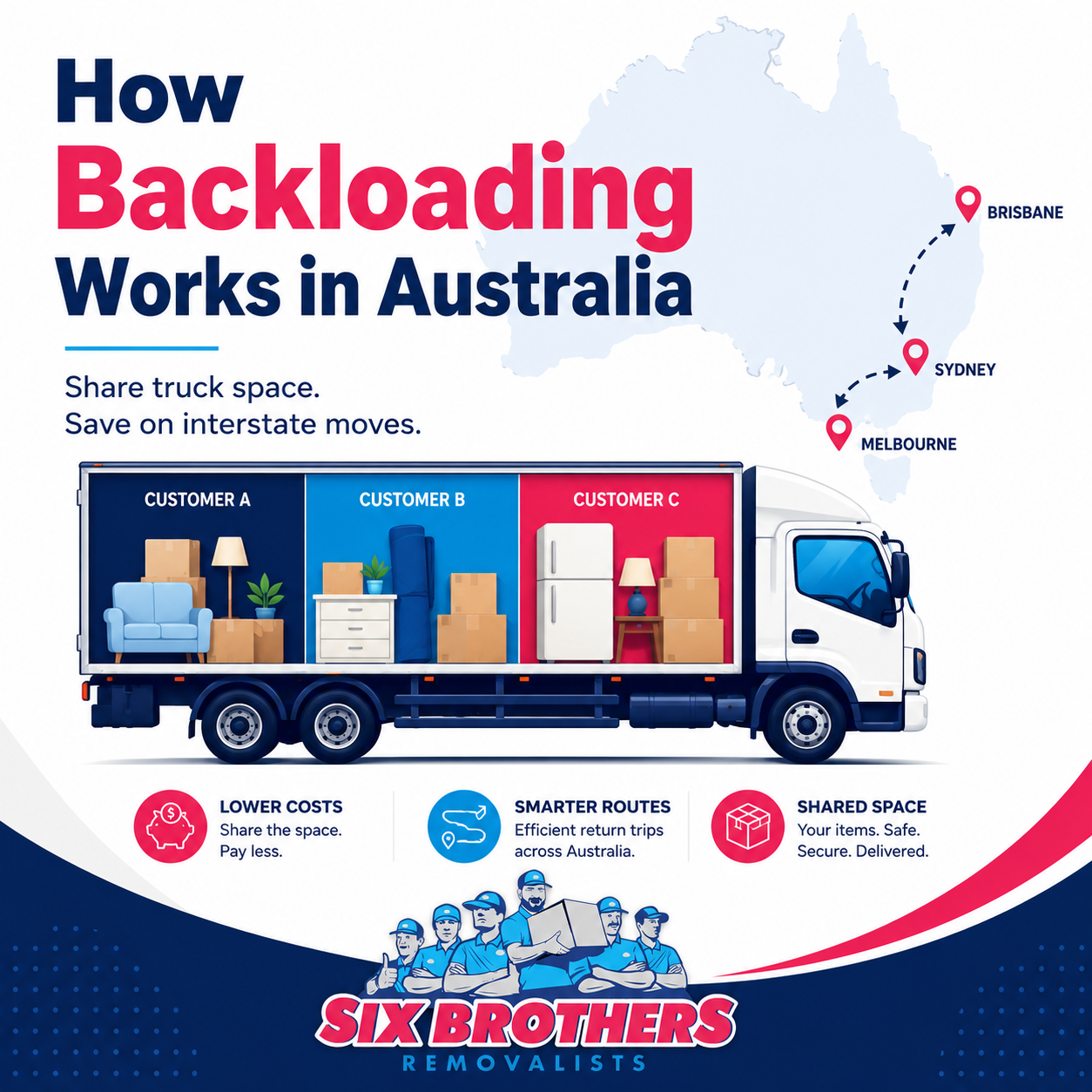

Interstate moves. $1,500 to $5,000+ depending on home size and distance. Backloading saves a lot.

Storage. $200 to $500 a month for a typical unit. Search “removalist and storage near me” for combined deals.

Moving boxes. $5 to $15 each. Bulk packs run cheaper. Or recycled ones are free if you look around.

Packers. Add $300 to $800 for full packers and movers sydney service. Worth it for big homes.

Insurance. $50 to $200 for transit cover. Don’t skip this for valuable stuff.

That’s the rough lay of the land. Numbers shift with size, distance, and timing. Always get three quotes before you book.

A Quick Word on Moving Lists and Address Updates

Moving needs paperwork too. A moving house checklist Australia covers most bases. Add a change of address checklist Australia for utilities, banks, and ATO updates. Both should be ready a month before move day. Last-minute panic costs money. Calm planning saves it.

Some keepsakes you don’t need to move. Furniture to keep when downsizing is the stuff that fits the new place. Donate or sell the rest. Less to move equals less to pay.

How to move without losing your mind? Start six weeks out. Sort by room. Label every box. Keep a “first night” box for essentials. Search “moving companies near me” or “removal companies near me” early. Good crews book out fast in peak season. Avoid the rush.

Why This Rule Helps Movers

We help people across Sydney every week. Six brothers and the team handle moves of all sizes. From studio apartments to big family homes. Office moves too. Need help with moving boxes? We’ve got those. Need movers and packers parramatta? Same. Long-distance like removalists sydney to brisbane? Yes.

Even tight runs like removalists wagga we sort out via partners. Tighter regional jobs need more planning. The 20% bucket makes that planning real. Cheap movers sydney crews fill up fast in peak months. So do removalists parramatta teams. Book early when you spot good rates.

Bottom line. The 70/20/10 budget rule is a solid starting point. It’s not magic. It won’t fix your finances overnight. But it gives you a frame to build on. Stick with it for three months. See how it feels. Adjust where needed. If you’re moving home soon, run the numbers first. Don’t get caught short. The cheapest moving plans still cost something.

For Sydney moves, give 6 brothers removalists a shout. Call 1300 764 372. Or email info@sixbrothersremovalist.com.au. Visit Suite 1 level 5/58/60 Macquarie St, Parramatta NSW 2150. We’ll help you plan, quote, and shift everything safely.

The rule is your map. The move is your journey. Pack smart, save smart, and you’ll land where you want.