Money fights are real. Especially when you’re moving house in Sydney or anywhere in Australia. Bills crawl in. Bond comes out. Truck quotes pile up. And payday feels miles away.

So how do you keep your wallet calm? You use a simple split. The 50/30/20 rule budget is that split. It’s a clean way to slice your pay packet. No spreadsheets that look like a maths exam. This guide answers what is the 50 30 20 rule in plain talk. We’ll walk through how it works. We’ll show you a 50/30/20 budget calculator example. And we’ll tie it back to real moves, real bills, and normal Aussie life.

You’ll learn how to use a moving budget planner with this rule. You’ll see a 50/30/20 budget template you can copy. And you’ll find out if the 60/30/10 budget rule fits you better.

By the end, you’ll know if it’s the right plan. Or if it’s just another shiny idea that doesn’t suit your wallet. Fair deal? Let’s go.

How the 50/30/20 Budget Rule Works?

The 50/30/20 rule explained is dead simple. You take your after-tax pay. Then you split it three ways.

Half goes to needs. A bit under a third goes to wants. The rest goes to savings or debt. That’s it. No fancy tricks. Senator Elizabeth Warren wrote about it in her 2005 book All Your Worth. The idea spread fast. Now folks in Parramatta, Dubbo, Wagga, and Wollongong use it daily.

It works because it’s easy to remember. And easy beats perfect every time. A budget you forget is a budget you’ve already lost.

50% Needs (Essential)

Half of your take-home pay covers needs. These are bills that keep your life ticking. Rent. Groceries. Power. Water. Petrol. Think of needs like the foundation of a house. Pull them out and the whole thing falls down. So they get the biggest slice.

If you’re moving, your removalist cost can land here too. Why? Because you can’t move without movers. Not many of us can lift a fridge solo.

The average removalist cost Australia families pay for a 3-bedroom move sits between $900 and $2,400. How much do removalists charge depends on size, distance, and time of week. Either way, it’s a need, not a want. You have to get from old place to new.

30% Wants (Discretionary)

Wants are the fun stuff. Netflix. Coffee runs. Friday takeaway. Footy tickets. New shoes you don’t really need. You get up to 30% for these. Spend less here and you free up cash fast. Spend more and your savings tank.

Wants aren’t bad. They’re what makes life feel like life. Just don’t let them eat your needs slice or drain your future.

20% Savings/Debt (Financial Goals)

The last fifth is for your future you. Emergency fund. Super top-ups. Credit card payback. House deposit. Moving costs you’re saving for. This bit gets skipped the most. People plan to save and then… payday vanishes. Sound familiar?

Treat this 20% like a bill. Pay yourself first. Set up an auto-transfer the day your wage hits.

What the 50/30/20 Rule Means for Your Budget?

So what does this rule actually mean for your wallet? It means clarity. You stop guessing where your money went. You start telling it where to go. It also means freedom inside fences. The fences are the three buckets. Inside each bucket, you choose. Want to spend your wants on books? Go for it. Want to spend on weekends out? Same deal.

For movers and packers Sydney families call every week, this rule is gold. They use it to plan their move. They save the 20% slice for months. Then they pay the truck, the boxes, and the bond cleaner.

Even if you’re hunting cheap movers Sydney prices, you still need a plan. The plan is what stops surprise bills from hurting. A surprise $400 storage bill stings less when you’ve got a buffer.

Why the 50/30/20 Budget Rule Works?

There’s an old Aussie saying. “She’ll be right, mate.” But she won’t be right if your budget’s a mess. The 50/30/20 rule works because it’s brain-friendly. Three numbers. One paycheck. Easy split.

Most budget plans fail for one reason. They ask too much. Track every cent. Log every coffee. Review every Sunday. Who has time for all that? This rule trims the fat. You don’t track 40 categories. You track three buckets. It also works because it leaves room. Room for fun. Room for mistakes. Room for life. A budget that’s too tight snaps. Like a rubber band stretched too far.

And it scales beautifully. A nurse in Parramatta can use it. A tradie in Dubbo can use it. A teacher who’s about to start a new gig can use it. Same rule, different numbers. That’s the magic.

50/30/20 Budget Example Calculation

Numbers help, right? Let’s run a real one. Say you take home $5,000 a month after tax. That’s a fair Aussie wage in 2026. You can plug these into any 50/30/20 budget calculator online. Or build your own 50/30/20 budget spreadsheet in Google Sheets. Both work fine.

Needs (50%)

Your needs slice is $2,500. That covers:

- Rent or mortgage: $1,800

- Groceries: $500

- Electricity and water: $200

Tight, but doable in many suburbs. In central Sydney, this might not stretch. In Wagga, Dubbo, or Orange, it stretches further. Move further out and your dollar grows legs.

Wants (30%)

Your wants slice is $1,500. That covers:

- Eating out: $300

- Streaming and gym: $80

- Hobbies: $200

- Date nights: $200

- Random shopping: $300

- Coffee and snacks: $120

- Buffer for fun: $300

Yes, this slice is bigger than people expect. That’s why the rule feels generous. Most folks in Sydney spend close to this without even noticing.

Savings (20%)

Your savings slice is $1,000. That covers:

- Emergency fund: $400

- Super contributions: $200

- Moving fund: $200

- Holiday fund: $200

If you’re planning a move, this $200 a month adds up fast. In a year, that’s $2,400. That covers most house removals jobs in NSW. The cost of moving a 3 bedroom house locally often lands right in that ballpark.

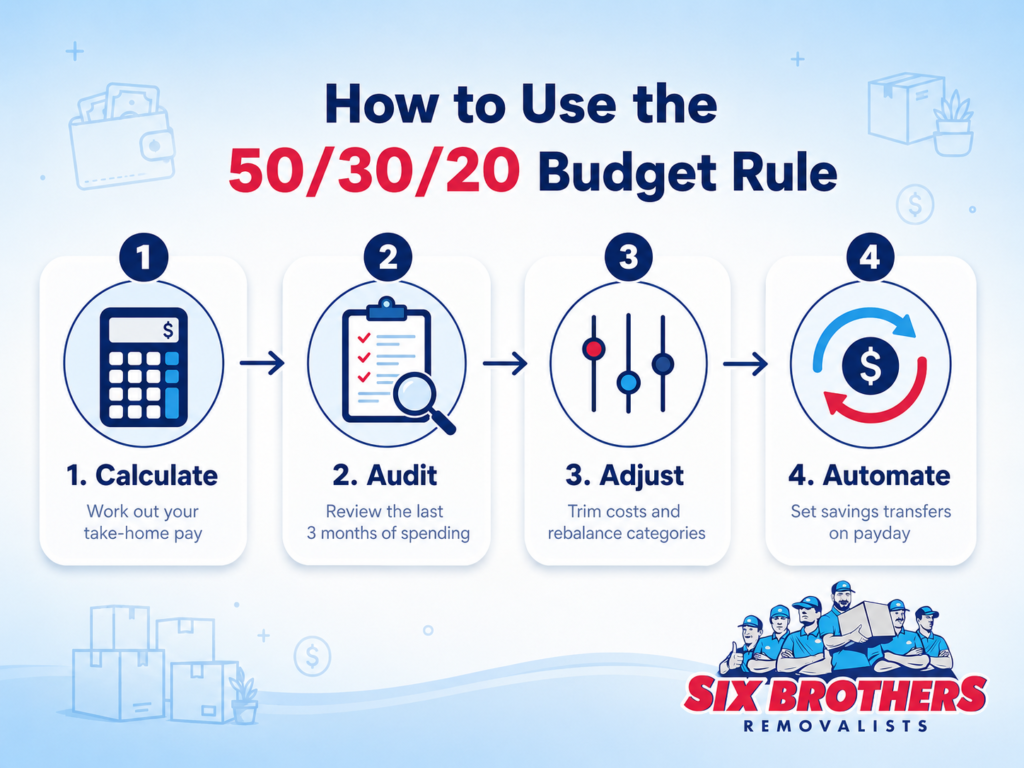

How to Use the 50/30/20 Budget Rule Step by Step

Talk is cheap. Let’s get hands-on. Here’s how to set up the rule today.

Calculate Take-Home Pay

Start with your net pay. Not gross. Net is what lands in your bank. Add up every income source. Wages. Side hustles. Rental income. Dividends. Total it for the month. Use a household budget calculator Australia banks offer free. Westpac, ANZ, and CommBank all have one. Or build a personal budget template Australia style in Excel. Both work.

For movers, also use a moving out budget calculator. It splits one-off costs from regular ones. Helpful when you’re juggling both.

Audit Your Spending

Pull up your last three months of bank statements. Yes, all of them. It’s painful but it’s the truth-teller. Sort each cost into one of the three buckets. Be honest with yourself. That weekly Uber Eats? It’s a want, not a need.

This step shocks most people. You’ll spot leaks. Subscriptions you forgot. Memberships you don’t use. Tap-and-go coffees that add up to $200 a month.

Adjust as Needed

Now compare your spend to the 50/30/20 split. Are you over on needs? Under on savings? Most folks are. Trim where you can. Switch energy plans. Cancel unused subs. Pack lunch a few days a week.

Don’t try to fix it in a day. Fix one thing per week. Slow change sticks. Fast change snaps.

Automate

This is the magic step. Set up auto-transfers on payday. 20% straight to savings. The needs amount stays in your main account. Wants go to a separate spending card.

When the wants card hits zero, you stop. No drama. No guilt. Your future you waves and smiles. That’s the whole game.

Needs vs Wants in the 50/30/20 Budget Rule

The line between needs and wants is fuzzy. That’s where most people trip and fall.

What Counts as Needs

Needs are things you must pay or your life breaks. No grey area here.

- Rent or mortgage

- Basic groceries

- Power, gas, water

- Petrol or transport for work

- Health insurance

- Phone (cheapest plan)

- Insurance (car, home contents)

- Childcare

- Minimum debt payments

If you’re moving, the truck and removalist costs land here. So does packing tape, basic moving boxes, and the bond on a new place. Even a basic moving house checklist Australia families follow lists these as essentials.

What Counts as Wants

Wants are nice but not vital. You’d survive without them.

- Streaming services

- Eating out

- New clothes (beyond basics)

- Holidays

- Hobbies

- Premium gym membership

- Top-shelf groceries (organic everything)

- Brand-name phone instead of basic

Even hiring two men and a truck for a small load can be a want if you could DIY. But for big moves, that’s a need. Not many of us can shift a fridge alone, like we said.

Where Debt Payments Fit

Debt is sneaky. Your minimum repayment is a need. Anything extra is a savings move. So the minimum credit card payment lives in the 50%. The extra $200 you throw at the balance lives in the 20%.

Same rule for car loans. Same for personal loans. Minimum is need. Extra is savings or debt killer. If you’re paying high-interest debt, lean harder. Push 25% or 30% to debt for a year. Then drop back. Pain now, peace later.

Different Names and Variations of the 50/30/20 Budget Rule

This rule has more names than my nan has casserole recipes. They all mean the same thing.

The 50-30-20 Rule

Some write it with dashes. Some with slashes. The 50-30-20 rule is the same as the 50/30/20 rule. Just different punctuation. Some search “50-30-20 rule” on Google. Some search “50/30/20 rule explained.” Same thing, different fingers.

The 50/30/20 Budgeting Method

A method is just a way of doing something. Calling it a method makes it sound official. The 50/30/20 budgeting method shows up in finance blogs and bank apps. It’s the same rule with a fancier hat.

The 50/30/20 Strategy

Some call it a strategy. That’s true too. A strategy is a plan with a goal. The goal here is balance. Bills paid. Life enjoyed. Future built. Three buckets, one strategy. Easy.

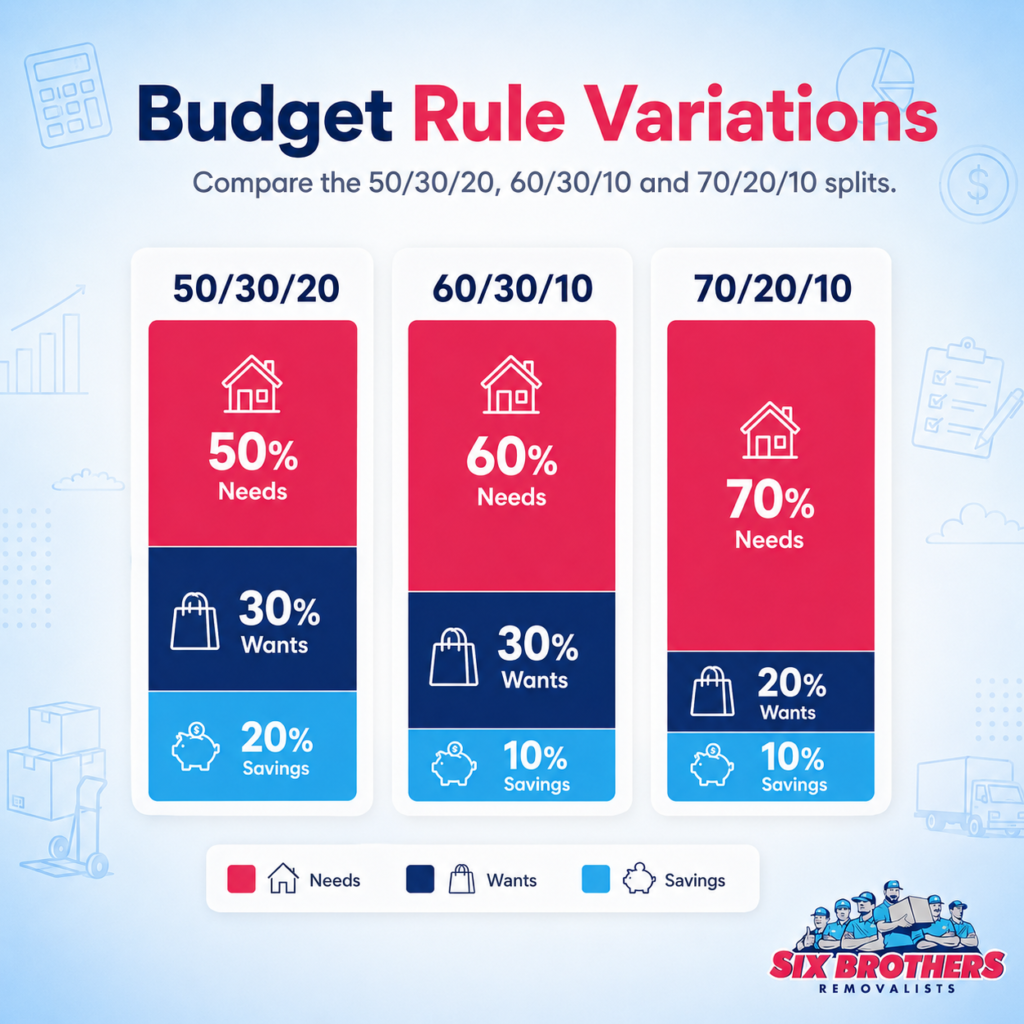

60-30-10 Variation

What if your rent eats your life? Then the 60/30/10 budget rule might fit better. You give 60% to needs, 30% to wants, 10% to savings. It’s not ideal, but it’s honest. Better to save 10% than zero.

This works for renters in Sydney. The median rent in inner suburbs eats half your pay alone. So the 60/30/10 is just real life on paper.

70-20-10 Variation

The 70-20-10 split is for tighter budgets. Most folks new to budgeting in Aussie cities can use this. 70% needs. 20% wants. 10% savings. It’s gentle. It’s a stepping stone.

You bump the savings up as your income grows. Or as your costs fall. The point is to start, not to be perfect day one.

Key Things to Consider Before Using the 50/30/20 Budget Rule

This rule isn’t a magic wand. It has limits. Be honest with yourself before you commit.

First, your income matters. If you earn close to minimum wage, 50% won’t cover your needs. Sydney rents are brutal these days.

Second, debt size matters. If you’re drowning in credit card debt at 22% interest, paying minimums isn’t enough. You may need 30% or more on debt for a while.

Third, life events matter. Are you moving? Having a baby? Caring for a parent? These tilt the buckets. A move alone can swallow a whole year of savings.

Fourth, location changes everything. Living in Parramatta costs different to living in Dubbo. The split should bend to your suburb, not the other way around.

Fifth, your goals matter. If you’re saving for a house deposit in two years, 20% might not be enough. You might need to push to 30% or 40%.

And sixth, your job stability matters. Casual workers and freelancers need a bigger emergency fund. Bump that 20% up if your income wobbles month to month.

The rule is a starting point. Not a finish line.

How to Adjust the 50/30/20 Budget Rule for Your Situation?

Life isn’t tidy. So your budget shouldn’t be either.

If you’re a young renter in Sydney, your needs slice may stretch to 60%. That’s fine. You’re not failing. You’re adjusting. If you’ve paid off your house, your needs slice might shrink to 30%. Bonus savings time. Push harder on the 20% bucket. If you’re moving soon, you might add a fourth bucket. Call it the moving fund. Pull from wants for a few months. The 20% goes to it instead of long-term savings.

Got a 4 week moving checklist to follow? Match it with a 4-week savings sprint. Each week, top up the fund. That covers boxes, packing tape, the truck, the cleaner, and a takeaway dinner on moving day.

Got kids? You may worry about the worst age to change schools or the worst age to move a child. Research says it’s tougher between ages 8 and 14. The best age to move a child is often before they start primary school. The worst age to change schools Australia parents flag is around year 7, that big primary-to-high jump.

But the budget rule still helps. A planned move with a clear money plan reduces stress for everyone.

If you’re moving away from family, a clear budget gives you confidence. You’ll know you can afford the trip back for visits. You’ll know you can afford the deposit on a new place. Family moved interstate last year? Same maths still works. The rule scales.

If you’re an expat looking up “verhuizen” or “demenagement” because English isn’t your first tongue, no stress. Whether you call it moving, verhuizen, or demenagement, the budget split stays universal. Three buckets. One paycheck. Same plan.

Use a moving house budget template alongside the rule. It keeps your moving fund honest. It also helps you compare removalist quotes side by side without losing track.

Is the 50/30/20 Budget Rule Right for You?

Honest answer? Maybe.

It’s a fantastic starting point. But it’s not for every wallet, every season, or every Sydney suburb.

Best for Beginners

If you’ve never budgeted, this rule is gold. Three buckets are easy to grasp. You can start today, even with your phone calculator.You don’t need apps. You don’t need spreadsheets. You don’t need a financial coach. Just a calculator and your last paycheck.

It’s also great for couples who’ve never combined finances. Three buckets are easier to argue over than 30 lines.

Good for Simple Money Management

For folks who hate fiddling, the 50/30/20 rule is the dream. Set it. Forget it. Adjust once a year. It’s the slow cooker of personal budgets. Simple ingredients, set the dial, walk away. Come back hours later and dinner’s ready.

If you’re already using a 50/30/20 budget planner or 50/30/20 rule calculator Australia banks provide, you’re halfway there. Just pair it with auto-transfers and you’re done.

When Another Method May Work Better

But it’s not perfect for everyone.

If you’re in deep debt, try the avalanche or snowball method. Pay highest interest first. Or smallest balance first. Whichever fires you up. If you’re chasing FIRE (financial independence retire early), this rule’s too soft. You may want a 50/20/30 flip. Or even 30/20/50, with savings as king. If your income changes every month, like a tradie or freelancer, you may need a percentage method tied to each invoice. Not flat monthly splits.

The point is, you can outgrow this rule. And that’s okay. Use it till it stops fitting. Then upgrade.

Pairing the 50/30/20 Rule With a Smart Move

Most people I chat with don’t budget for moving. They wing it. Then they cry when the truck quote lands. Don’t be that person. Use the 50/30/20 rule and a moving budget planner together. Save 20% for three months and you’ve got real cash for boxes, movers, and the bond.

Need help knowing how to reduce moving costs? Three quick wins:

- Compare removalist quotes from at least three companies before booking

- Move midweek, not Saturday, for cheaper rates

- Pack non-fragile stuff yourself and let pros handle the heavy gear

Wondering when to start packing before moving? Four weeks out is the sweet spot. That matches a standard moving day checklist. Start with stuff you don’t use daily. Books, off-season clothes, decor. Don’t forget the change of address checklist Australia essentials. Update Medicare, ATO, electoral roll, banks, super fund. Most of this is free. Some take five minutes online.

If you’re downsizing, ask yourself the hard question. Which furniture to keep when downsizing and which to sell or donate? The sofa you bought during uni might not fit your new life. Be ruthless. Lighter loads cost less to move.

Final Thoughts

The 50/30/20 rule isn’t perfect. Nothing is. But it’s a clean, simple frame for a messy thing called money. Use it for groceries. Use it for rent. Use it for a move you’ve been putting off. Three buckets. One paycheck. One plan that grows with you.

If your move is in Sydney, Parramatta, Dubbo, Wagga, or anywhere across NSW, Six Brothers Removalists can help. We’re known for cheap removalist Sydney rates and full-service packers and movers Sydney trusts. Whether you need a quick studio shift or a full interstate haul, we’ve got the truck and the team.

Call us on 1300 764 372. Email info@sixbrothersremovalist.com.au. Or pop by Suite 1 Level 5/58/60 Macquarie St, Parramatta NSW 2150.

Plan smart. Move smart. And let your budget do the heavy lifting before we do.

Frequently Asked Questions

Is the 50/30/20 rule realistic in Sydney?

For some, yes. For renters in inner suburbs, the 60/30/10 split works better. Adjust the rule to your real life. Don’t force the rule on a rent you can’t change.

Should I include super in my 20% savings?

Compulsory super doesn’t count, since it comes out before you see your pay. But extra voluntary contributions do. They count as savings.

Can I use this rule if I’m self-employed?

Yes, but pay yourself a steady “wage” each month. Apply the rule to that. Keep business income and personal split clear.

What’s the best free 50/30/20 budget template?

Most major Aussie banks offer one. So does Moneysmart.gov.au. Or build a quick 50/30/20 budget spreadsheet in Google Sheets. Three rows, three columns, done.

Does the rule work for retirees?

Sometimes. If your home is paid off, needs drop. You can flip the rule to 30/30/40 with savings going to long-term care or holidays.