Ever wondered why some sellers pocket way more cash than others? It’s not luck. It’s timing, paperwork, and knowing the rules. In Australia, the Australian Taxation Office (ATO) plays by a clear rule book. But clear doesn’t mean easy. Miss one step and you hand back thousands.

This guide breaks it all down. No jargon. No fluff. Just the stuff that saves you money. We’ll cover capital gains tax investment property Australia rules, main residence exemptions, and smart moves before you list. By the end, you’ll know what to do, when to do it, and what to skip.

Ready? Let’s crack on, mate.

Key Capital Gains Tax Rules for Selling an Investment Property in Australia

Capital gains tax, or CGT, is the tax on profit when you sell. It’s not a separate tax. It gets added to your taxable income that year. Think of CGT like a toll at the end of the road. The ATO wants its cut. Your job is to pay what’s fair, not a cent more.

Here are the rules that matter most.

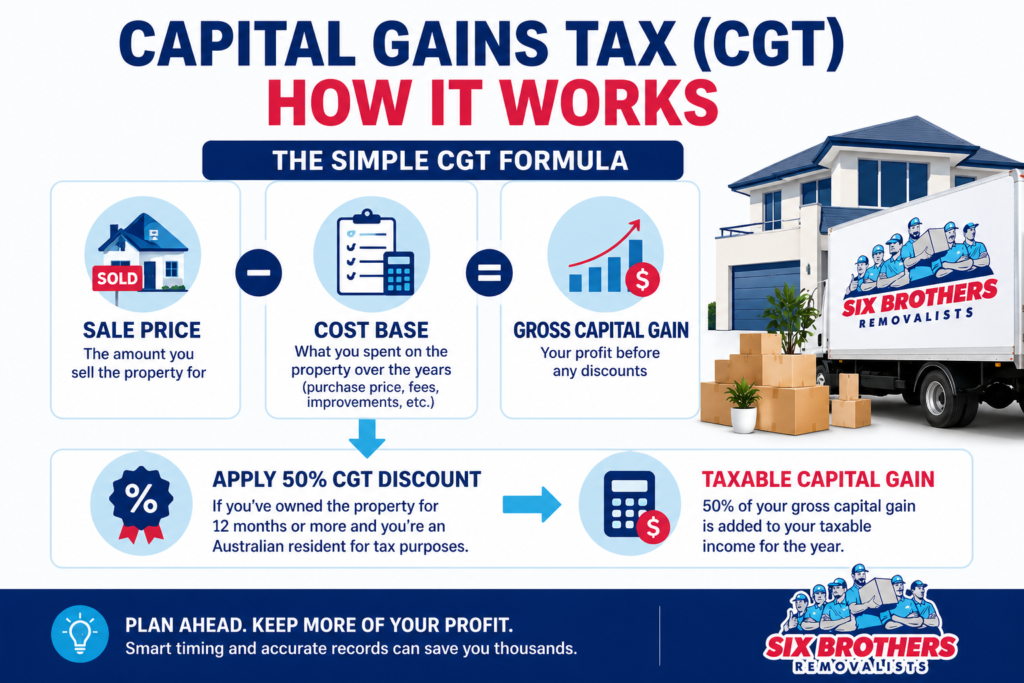

50% CGT Discount

If you own the property for 12 months or longer, you get a 50% discount. That means only half the gain gets taxed. You need to be an Australian resident for tax. Companies miss out on this one. Individuals and trusts (with rules) can use it.

Hold for 11 months? You pay tax on the full gain. That one month can cost thousands. Timing matters.

Cost Base Adjustments

Your cost base is what you spent on the property over the years. A bigger cost base means smaller gain. It includes:

- Purchase price

- Stamp duty

- Legal and conveyancing fees

- Building inspection and pest reports

- Capital improvements (new kitchen, extension, decking)

- Loan setup costs in some cases

But wait. You must subtract any depreciation claimed as a rental. And repairs don’t count as improvements. Fixing a leaky tap? Not here. New roof? That’s capital.

Contract Date Matters

The CGT event happens on the contract signing date. Not settlement. Not handover. So if you sign on 29 June and settle on 15 July, the gain sits in the earlier financial year. That one date swings your whole tax bill.

Plan this with your accountant. A week can shift the gain into the next year.

Six-Year Rule (Absence Rule)

This one is gold. If the property was your main residence first, you can rent it out for up to six years. You still keep the main residence exemption. You must not claim another property as your main home during that time. Move back in before six years? The clock resets. You get another six-year stretch. Two quick rules:

- Must have been your actual main home before renting

- Only one main residence at a time (mostly)

Moving In To Reduce Tax

Moving into your rental before selling can cut your CGT. But it’s not a magic switch. The ATO wants proof you really lived there. You get a partial exemption for the time it was your main home. The rest of the ownership stays taxable. We’ll break this down later with numbers.

Calculating Gain

The formula is simple. Sale price minus cost base equals gain. Then apply the 50% discount if you qualify. Then add that number to your taxable income for the year. Quick example:

- Sale price: $900,000

- Cost base: $600,000

- Raw gain: $300,000

- After 50% discount: $150,000

- Added to your income that year

If your income puts you in the top bracket, that $150,000 gets taxed at up to 47%. Ouch. That’s why planning pays.

Main Residence Exemption

Your own home is usually CGT-free. This is called the main residence exemption. It’s the biggest tax break most Aussies ever get. But it only works if the home was truly your main home. Renting it out changes things. Using part of it for business changes things.

Full exemption needs full-time main residence use. Partial use means partial tax.

Rules for Transitioning From an Investment Property to a Main Residence

Going from rental to main home can save tax. But it takes more than a couch and a kettle. The ATO has a checklist.

Moving into a Rental

You need to actually live there. That means:

- Change your address on the electoral roll

- Update your driver’s licence

- Redirect mail

- Move utilities into your name

- Sleep there most nights

Tip: Keep receipts, bank statements, and bills. If the ATO asks, you need to prove it. Not assume it.

Constructing a New Home

Bought vacant land to build on? There’s a four-year rule. You can treat the land as your main residence while you build. But only if you move in once it’s done and live there for at least three months.

This helps buyers who knock down and rebuild. Or first home builders. Don’t skip the three-month rule. That’s where people trip.

Records Retention

Keep every record for five years after the CGT event. Contracts, receipts, invoices, emails, inspection reports. All of it. If you claim the six-year rule or a partial exemption, keep even longer. The ATO has a long memory, like an elephant.

Folder it all. A cheap ring binder beats a panicked tax time.

Moving In Before Selling vs Selling Before Moving for Tax Purposes

This is the big choice. Sell now or move in first? Both have tax outcomes. Both have lifestyle costs. Let’s weigh them up.

Selling Before Moving

You sell the rental while it’s still a rental. Full CGT applies. The 50% discount still works if held 12+ months.

Pros:

- Simple and fast

- Clear money to buy next home

- No awkward in-between move

Cons:

- No main residence exemption on this sale

- Full gain taxed (after discount)

If your gain is small, this can be the cleanest path. No mess. No waiting.

Moving In Before Selling

You move in. Make it your main residence. Then sell later. The time it was a rental stays taxable. The time as your main home gets exempt. That’s the split.

Pros:

- Lower CGT overall

- You get to enjoy the home

- Can use six-year rule if you leave again

Cons:

- Takes time to set up as main home

- Needs real evidence

- May delay your next move

There’s no single answer. It depends on your gain, your income, and your timeline.

Pro-rata CGT

The ATO uses a days-based formula for partial exemptions.

Formula: Taxable gain = Total gain × (Days as rental ÷ Total days owned)

Example:

- Owned 10 years (3,650 days)

- Rented for 6 years (2,190 days)

- Main home for 4 years (1,460 days)

- Total gain: $400,000

- Taxable portion: $400,000 × (2,190 ÷ 3,650) = $240,000

- After 50% discount: $120,000

That $120,000 is added to your income. Better than the full $400,000 getting smacked.

Evidence of Residency

The ATO loves paperwork. Here’s what counts:

- Electoral roll registration at the address

- Driver’s licence updated

- Utility bills in your name

- Mail redirection

- Home insurance as owner-occupier

- Medicare and bank records

A weekend crash pad doesn’t cut it. You need to live there. Nights, meals, mornings. The works.

Can You Have More Than One Main Residence for CGT Purposes in Australia?

Short answer: usually no. The ATO lets each family have one main residence at a time.

But there’s a six-month overlap rule when moving. You can treat two homes as main residences for up to six months. Handy when buying a new place before selling the old one. Conditions apply:

- Old home must have been your main residence for 3+ continuous months in the 12 months before sale

- Must not have been rented during those 12 months

- Sale must settle within six months of buying the new home

Couples can’t pick one main residence each. Spouses must share one main residence or split the exemption. This trips up plenty of people.

What Happens for Tax If You Sell an Investment Property Before Moving In?

You sell it as an investment property. Full stop.

That means:

- No main residence exemption

- CGT applies to the full gain

- 50% discount if held 12+ months as individual

- Taxed at your marginal rate

No grey area here. If you never lived in it as your main home, it stays a rental in the ATO’s eyes.

What helps:

- Strong cost base (include every legit cost)

- Capital losses from other assets

- Split ownership between spouses

- Sell in a lower-income year

Ever sold shares at a loss? Those losses can offset your property gain. Don’t leave them on the table.

Sydney-Specific Property Tax Considerations When Selling Before Moving

Sydney isn’t a regular property market. It’s a beast of its own. The prices, the rules, the buyer pool all different.

Property price impact

High prices mean high gains. That means high CGT bills. A $500k rental bought in 2012 might sell for $1.3m today. The gain alone could push you into the top tax bracket for that year.

Plan sale timing around your income. Retiring soon? Take a career break? A year with lower income can save tens of thousands.

Stamp duty factors

Stamp duty isn’t CGT. But it affects your next move. NSW stamp duty on a $1m purchase is around $40,000 for owner-occupiers. Buying your new home before selling? You may face double holding costs. Land tax. Stamp duty. Loan interest. Budget for it.

First home buyers may get stamp duty concessions in NSW. Check revenue.nsw.gov.au for updates.

NSW regulations

NSW has land tax on investment properties above the threshold. It’s state tax, not federal. But it affects your holding cost and cost base. Land tax paid on investment years adds to your cost base if not claimed elsewhere. Keep every notice. Every receipt. Every year.

When it’s time to move house, you’ll want Sydney removalists locals trust. Six Brothers Removalists has been doing this for years.

How to Reduce Capital Gains Tax Legally

Let’s get practical. Here are legit ways to shrink your CGT bill.

1. Hold for 12+ months. The 50% discount is the easiest win. If you’re close, wait a few weeks.

2. Offset with capital losses. Sold loss-making shares? Old crypto in the red? Use those losses against your property gain.

3. Contribute to super. Concessional super contributions reduce taxable income. That includes your capital gain. Limits apply (currently $30,000 per year).

4. Time the sale. Sell in a low-income year. Maternity leave, career break, or retirement year can slash your marginal rate.

5. Split ownership. If held jointly, each owner reports half the gain. Two lower brackets beat one top bracket.

6. Use the six-year rule. If it was once your main home, rent it for up to six years and stay exempt.

7. Build the cost base. Include every legit cost. Stamp duty, improvements, legal fees, borrowing costs. Don’t underclaim.

8. Claim depreciation wisely. Depreciation lowers rental income tax. But it also lowers cost base. Weigh both sides.

Why give the ATO more than it needs? A good accountant earns their fee on one sale alone.

Common Tax Mistakes When Selling an Investment Property Before Moving

People lose thousands to simple slip-ups. Here are the big ones.

Missing the 12-month mark. Selling at 11 months loses the 50% discount. A month of patience can save serious cash.

Forgetting cost base items. Stamp duty, legals, improvements, inspection fees. Many sellers forget half of it.

Claiming main residence without proof. The ATO asks questions. Vague memories don’t count. Keep records.

Ignoring contract date. Gain goes to the year you signed, not settled. This changes your tax year.

Not reporting overseas buyers’ clearance. Sellers over $750k must give buyers a clearance certificate. Miss this and buyers withhold 15%.

Double-dipping depreciation. You can’t claim depreciation and ignore it in the cost base. Pick a lane.

Skipping capital losses. Got losses somewhere? Use them. They don’t expire.

Trying to split main residence with your spouse. You can’t. One household, one main residence.

“Ask twice, cut once” — old bushie wisdom. Same goes for tax. Ask your accountant before you sign.

Reporting Capital Gains Tax and Property Sale Deductions

You report your gain in your tax return for the year of the contract date. The gain goes into the income section. Most online tax software has a CGT worksheet. Fill it in with:

- Sale price

- Cost base

- Dates

- Discount claimed

- Main residence use (if any)

If your records are solid, this takes an hour. If not, it takes a week and a headache.

Capital Losses

Capital losses from other assets can offset your gain. That’s the same year or carried forward from earlier years. Important: apply losses before the 50% discount, not after. This maximises your deduction.

Example:

- Gain: $200,000

- Capital loss from shares: $50,000

- Net gain: $150,000

- After 50% discount: $75,000

If you apply the discount first, you only use $25,000 of losses. Big difference.

Clearance Certificates

Selling for $750,000 or more? You need a foreign resident capital gains withholding clearance certificate from the ATO. It’s free. It’s online. It takes a few days. Without it, the buyer must hold back 15% of the sale price and send it to the ATO. You get it back later, but it’s a cash flow mess.

Apply early. Like a month before settlement. Don’t leave it to the last week.

Step-by-Step Tax Planning Before Selling an Investment Property

Here’s a clean order of operations. Run through this before you list.

Assess property status

Work out the tax status of your property. Is it:

- An investment the whole time?

- Once your main home, now rented?

- Recently moved into?

Each one has a different tax path. Write down the history. Dates in, dates out, rental start, rental end.

Mini checklist:

- Purchase date and price

- Periods as main residence

- Periods rented

- Improvements and dates

- Any six-year rule use

Calculate gain

Add up the cost base. Work out the likely sale price. Subtract one from the other. That’s your raw gain. Apply the 50% discount if held 12+ months. Apply any partial main residence exemption.

This gives you the taxable gain. Add it to your expected income for the year. That tells you the tax hit. Use the ATO’s CGT calculator online for a quick estimate. Or ask your accountant for a proper model.

Choose strategy

Based on the numbers, pick your move:

- Sell now if gain is small or income is low

- Move in first if gain is big and you can actually live there

- Delay one year if you’re close to the 12-month mark

- Split across years if a sale straddles financial year end

- Use super if you can carry forward concessional caps

Once you pick, set dates. Book the accountant. Line up the real estate agent. And book your removalists early. Good movers get booked out weeks ahead.

Planning Your Move After the Sale

Once the tax side is sorted, the move is next. This is where the real work starts.Whether you’re heading across town or across states, movers matter. A bad move can ruin a good sale. Scratched floors. Lost boxes. Late arrivals. Not what you need after a long property journey.

Six Brothers Removalists handles it all. From small studios to big family homes. From local runs in Parramatta to interstate jobs across the country.

What we cover:

- Local Sydney jobs, including cheap movers sydney coverage

- Country NSW moves like Dubbo and Wagga

- Interstate runs: Sydney to Melbourne, Brisbane, Adelaide

- Short hops like Sydney to Wollongong or Gosford

- Packing and storage services

Need a quick in-and-out for a studio? Try our speedy van service. Moving a full house? We scale up the team.

Our rates are fair. The hourly rate for removalists at Six Brothers is competitive across Sydney. No hidden fees. No surprise charges.

Call us on 1300 764 372 or email info@sixbrothersremovalist.com.au. We’re at Suite 1 Level 5/58-60 Macquarie St, Parramatta NSW 2150.

Final Thoughts

Tax rules on selling an investment property sound scary. They’re really just a set of steps. Know your cost base. Watch the 12-month mark. Understand the six-year rule. Keep your records. Plan the contract date. And use every legal deduction you can find.

Then sell smart and move smart. A good move starts with a good plan and good movers. Ready to sell, pack up, and head to your next place? The Six Brothers crew is ready when you are.