So you’ve been sitting on a chunk of home equity. Maybe the kitchen looks like it belongs in a 1998 sitcom. Maybe the credit card bill is starting to feel like a second mortgage on its own. Either way, a $60,000 home equity loan keeps popping into your head.

But the big question? How much will you actually pay each month?

Here’s the truthful answer most banks won’t shout from the rooftop. The monthly payment depends on the rate, the term, your credit, and how lenders feel about your suburb that week. As the old Aussie saying goes, “she’ll be right” only works if the numbers are right first.

Let’s break it down properly. No jargon. No fluff. Just real figures and a clear path forward, especially if you’re moving soon and weighing up your options in Sydney.

Estimated Monthly Payment on a $60,000 Home Equity Loan

Quick numbers first. Then we’ll go deeper. A $60,000 home equity loan in Australia usually runs between 7% and 9% interest. Terms commonly land at 10 or 15 years.

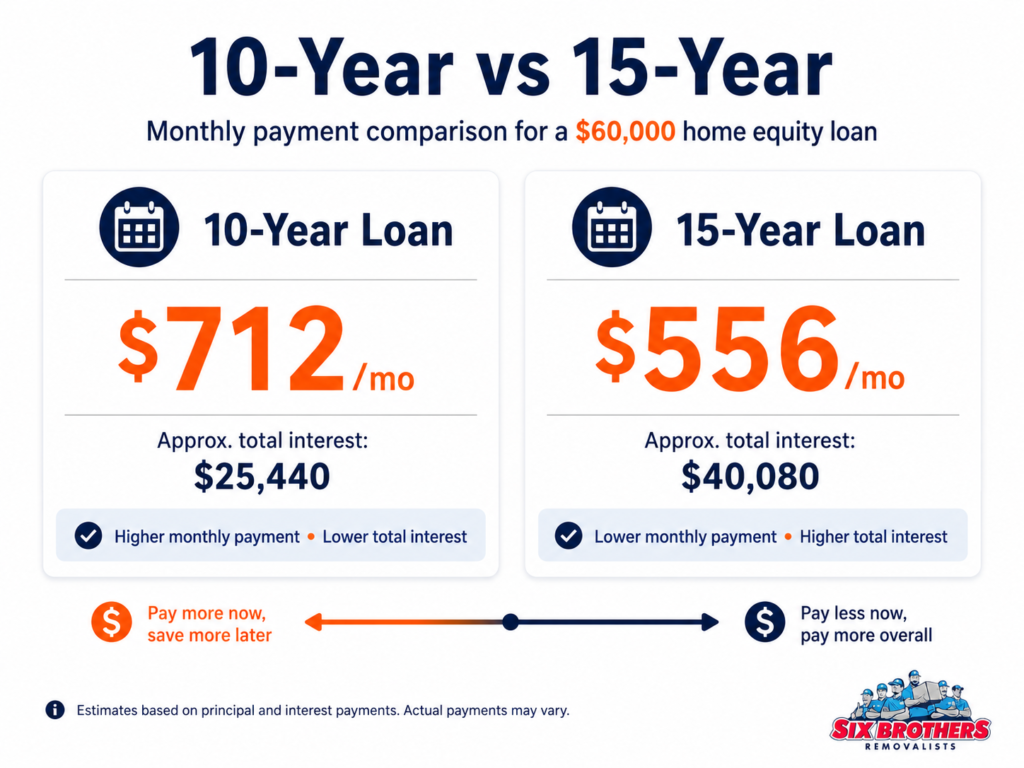

The shorter the term, the higher the monthly payment but lower the total interest. Simple as that. Below you’ll see what your payment looks like across four real-world scenarios. These figures use standard principal and interest calculations.

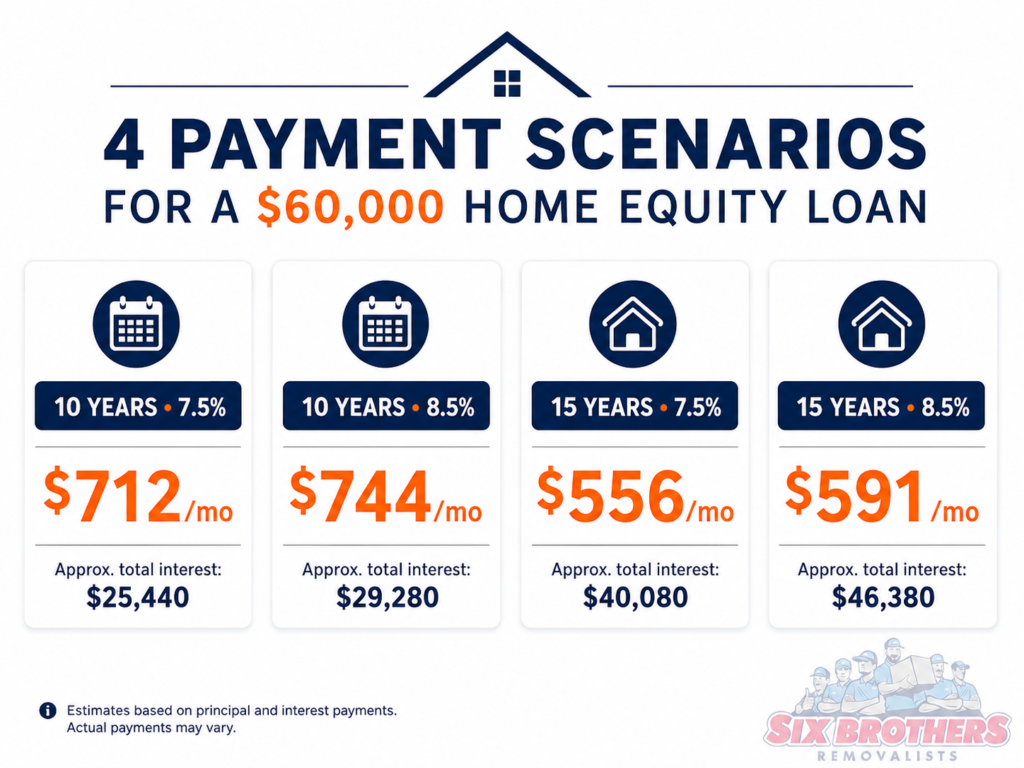

10 Years at 7.5%

At 7.5% over 10 years, you’re looking at around $712 per month. Total interest over the life of the loan? Roughly $25,440.

That’s a tidy option if you want the debt gone fast. You feel the pinch monthly. But you save big on interest. Ten years passes quicker than you think when you’re busy raising kids or scaling a business.

10 Years at 8.5%

Bump the rate to 8.5% and the monthly payment climbs to about $744. Total interest paid hits close to $29,280. So a 1% rate jump costs you nearly $4,000 over the term. That’s a family holiday gone. Rate shopping matters more than most people realise.

15 Years at 7.5%

Stretch it to 15 years at 7.5% and the payment drops to roughly $556 per month. But total interest balloons to around $40,080.

Lower payment. Higher total cost. It’s a trade-off. Some folks love the lower monthly hit because cash flow feels easier. Others hate the idea of paying so much interest. Both views are fair.

15 Years at 8.5%

At 8.5% over 15 years, expect to pay about $591 monthly. Total interest? Close to $46,380.

That’s almost as much in interest as the original loan amount. Ouch. This is why your credit score and lender choice matter so much. A small rate change creates a huge dollar difference over time.

What Affects the Monthly Payment on a $60,000 Home Equity Loan?

Five things move the needle. Get these right and you save thousands.

Interest Rates

Rates are the loudest factor. They swing with the Reserve Bank of Australia’s cash rate. They also swing with how lenders see risk in your loan file. Even a 0.25% drop saves you serious money. Always ask for the comparison rate, not just the headline rate. The comparison rate includes fees that sneak up later.

Loan Term

Short term, high payment, low total cost. Long term, low payment, high total cost.

That’s the rule. Pick your poison based on your cash flow. If you’re moving house soon, think hard about the term. A 15-year loan tied to a home you’ll sell in 5 years can get messy.

Credit Score

Your credit score is basically your money report card. Banks love a clean one.

A score above 750 in Australia usually gets you the best rates. Below 600? You’re paying premium pricing or getting knocked back. Pay your bills on time. Don’t apply for ten cards at once. Check your file before you apply for the loan.

Loan-to-Value (LTV) Ratio

LTV is the loan amount divided by the home value. Lower is better.

Most lenders want LTV below 80% for home equity loans. If your home is worth $1 million and you owe $500,000, your LTV is 50%. That’s healthy. Higher LTV means higher rates. Or it can mean lenders mortgage insurance on top.

Home Equity Calculators

Don’t guess. Use a home equity calculator before you walk into any bank. Punch in your home value, current mortgage balance, and desired loan amount. The calculator spits out borrowing capacity and rough monthly payments.

It takes 60 seconds. It saves hours of confusion. Some calculators even compare lenders side by side. Just like a Moving Home Calculator helps you budget your relocation day, an equity calculator tells you exactly what you can borrow.

How to Get a Low-Rate Home Equity Loan in Sydney

Sydney lenders are competitive. That’s the good news. The bad news? They’re picky too.

Here’s how to stack the odds in your favour:

- Shop at least four lenders. Big four banks, neobanks, credit unions, mortgage brokers. Each one prices differently.

- Get your paperwork in order before applying. Payslips, bank statements, council rates notice, home insurance proof.

- Improve your credit file 3 months before applying. Pay down cards. Avoid new credit enquiries.

- Ask about fixed vs variable. Fixed gives stability. Variable can save money if rates drop.

- Negotiate. Always negotiate. Banks have flexibility most people never ask for.

A good mortgage broker often beats walking into a branch yourself. They know which lender is hungry for your loan type this month.

$60,000 Home Equity Loan Payment Table by Rate and Term

Numbers laid out clean. So you can scan and compare.

10-Year Loan Costs

| Rate | Monthly Payment | Total Paid |

| 6.5% | $682 | $81,840 |

| 7.0% | $697 | $83,640 |

| 7.5% | $712 | $85,440 |

| 8.0% | $728 | $87,360 |

| 8.5% | $744 | $89,280 |

| 9.0% | $760 | $91,200 |

15-Year Loan Costs

| Rate | Monthly Payment | Total Paid |

| 6.5% | $523 | $94,140 |

| 7.0% | $539 | $97,020 |

| 7.5% | $556 | $100,080 |

| 8.0% | $573 | $103,140 |

| 8.5% | $591 | $106,380 |

| 9.0% | $608 | $109,440 |

Total Interest Paid

This is where the term decision really shows its teeth. At 7.5%, a 10-year loan costs $25,440 in interest. The 15-year version costs $40,080. That’s a $14,640 difference for the same loan amount.

Ask yourself: is the lower monthly payment worth nearly $15K extra? For some people, yes. For others, no chance.

How a Home Equity Loan Works

A home equity loan lets you borrow against the value you’ve built up in your home. The bank gives you a lump sum. You pay it back in fixed monthly chunks. It sits as a second loan behind your main mortgage. Your home is the security. Miss payments and the lender can act on the property.

Equity is the difference between your home’s market value and what you still owe. If your house is worth $1.2 million and you owe $700,000, you have $500,000 in equity. Most lenders let you tap up to 80% of the home value, minus your existing mortgage. So for that example, the maximum total borrowing would be $960,000. Subtract the $700,000 mortgage. You could borrow up to $260,000 in equity. Plenty of room for a $60,000 loan.

The funds land in your bank account. Use them however you like. Renovation, debt payoff, deposit on the next place, school fees, anything. Just remember, you’re trading future cash flow for present cash today.

Sydney Home Equity Loan Costs and Borrowing Context

Sydney is its own beast. Property prices, lender appetite, and borrower pressure all play differently here than in other capitals.

Sydney Mortgage Costs

The median Sydney house price sits around $1.4 million in 2025. Mortgage repayments on a typical loan eat up a hefty share of household income. Adding a $60,000 home equity loan on top means you need real budget headroom. Lenders will stress-test your servicing capacity. They want to see you can still pay if rates rise by 3%.

NSW Homeowner Data

Roughly 65% of NSW households are homeowners or paying off a mortgage. Many sit on substantial equity, especially those who bought before 2015. That’s why home equity loans are popular here. People have built wealth in their bricks. They want to put it to work without selling up and moving.

Local Borrowing Pressure

Sydney homeowners face rising rates, rising costs, and rising school fees. Many use equity to bridge gaps. But borrowing pressure is real. Don’t borrow more than you can service comfortably. A buffer of 3 to 6 months in savings is smart before taking on extra debt.

If a move is on the horizon, factor in costs like stamp duty, conveyancing, and removalists. The whole picture matters, not just the loan. If a move is on the horizon, factor in costs like stamp duty, conveyancing, and removalists. See our Sydney removalist costs full breakdown to plan the moving day spend properly.

Home Equity Loan vs Refinance

Loan or refi? Most people get confused here. Let me unpack it.

Equity Loan Top-Up

A top-up adds money to your existing home loan. You keep the same lender. You get extra cash at your current mortgage rate. It’s often the simplest path. Less paperwork. Same monthly direct debit, just bigger.

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a new, larger one. You take the difference in cash. This works well when rates have dropped since you locked your original loan. You get cash plus a lower overall rate. Two wins for the price of one.

Redraw Facility

A redraw lets you pull back extra payments you’ve made on your mortgage. No new application. No new loan. But the funds available depend on how much extra you’ve paid. Most homeowners don’t have $60K sitting in redraw.

Offset Account Access

An offset account holds money that reduces the interest charged on your mortgage. You can withdraw at any time. If you have $60K in offset, just use it. You’ll save interest and avoid taking on a new loan. Why pay 8% to borrow your own money?

How to Calculate Monthly Payments on a $60,000 Home Equity Loan

Want to do the maths yourself? Here’s the simple formula lenders use:

M = P × [r(1+r)^n] / [(1+r)^n – 1]

Where:

- M = monthly payment

- P = loan amount ($60,000)

- r = monthly interest rate (annual rate ÷ 12)

- n = total number of payments (years × 12)

Let’s plug in 7.5% over 10 years. The monthly rate is 0.625%. The number of payments is 120. Run the formula and you get $712.05 per month. Match what we showed earlier.

You don’t need to memorise this. Any home equity calculator does it instantly. But knowing the formula helps you trust the numbers when a bank shows them to you.

Common Ways Sydney Homeowners Use $60,000 in Home Equity

Sixty grand goes further than you think. But where most people put it tells a story.

Home Renovations

Kitchens, bathrooms, and outdoor spaces dominate the list. A mid-range kitchen reno in Sydney costs $30,000 to $45,000. A bathroom sits around $20,000 to $30,000. Sixty thousand can fund both. Done well, these renos add real value. Done poorly, you’ve spent the money and barely lifted the price.

If you’re planning to sell soon, focus on low-cost upgrades that add value before moving. Don’t overcapitalise. Want to push your home’s price higher before you list? See our guide on how to add $100K value before selling and moving for the smart spend list.

Debt Consolidation

Credit cards at 21% interest are wealth killers. Personal loans at 14% are not much better.

Rolling those into a home equity loan at 8% saves serious cash. Just don’t run the cards back up after. That’s the trap most people fall into.

Pair the consolidation with a cancelled card or two. Use cash or debit instead. Lock in the savings.

Investment Property Deposit

Sixty grand can be a deposit on an investment property in regional NSW. Towns like Dubbo, Wagga, Orange, and Port Macquarie still offer entry points under $600,000. Rental yields in regional areas often beat metro. But always check vacancy rates and growth history first. Investment property is a long game, not a punt.

Major Life Expenses

Weddings, school fees, medical bills, business start-ups, family support. Life happens. Equity helps cover the big stuff without raiding super. Just remember: equity is real money you’ve earned. Treat it that way. Borrow only what serves the next chapter, not the last regret.

If you’re planning a move alongside this loan, a furniture removalist team that knows Sydney inside out makes the day a thousand times smoother. We get it. Money’s tight when you’re juggling renovations, loans, and relocation. That’s why we keep it real, keep it priced fair, and keep your stuff in one piece.

Ready to Move After Tapping Your Equity?

Phone: 1300 764 372 Email: info@sixbrothersremovalist.com.au Address: Suite 1 Level 5/58 Macquarie St, Parramatta NSW 2150

Six Brothers Removalists has helped Parramatta and greater Sydney families move into their next chapter for years. Whether you’re renovating, downsizing, or shifting interstate after pulling equity, we’ll handle the heavy lifting. Literally.

Give us a call. We’ll talk straight, quote fair, and get you moved.