So you’ve heard about the 28/36 rule and now you’re wondering, what’s the big deal?

Short answer. It’s a budgeting yardstick that keeps your home loan from eating your life. Spend up to 28% of your gross monthly income on housing. Keep total debt under 36%. That’s the whole idea.

In Australia, this rule is a borrowing sanity check. Banks don’t quote it on every brochure. Yet it shapes how much mortgage you can afford Australia-wide. It also shapes how smoothly your moving day goes.

Here’s the catch. Sydney prices punch hard. The 28/36 rule sometimes feels like trying to fit a queen mattress through a studio door. So you need to bend it without breaking your budget. This guide breaks it down. Plain words. Real numbers. A few Sydney truths your bank won’t shout about.

Ready? Let’s roll.

How the 28/36 Rule Works for Home Buyers

Picture your pay slip. Now slice it into two pies. One pie covers the roof. The other pie covers everything you owe. The 28/36 rule sets the limits. It’s a household budget capacity rule. Lenders love it. Buyers should respect it.

The 28% Rule (Housing)

The first number. 28% of gross monthly income should cover housing only. That means mortgage repayments, council rates, insurance, and strata fees if any. Why 28%? Because rent or mortgage is your biggest fixed cost. Going over 28% squeezes everything else.

Quick math. Earn $8,000 a month gross? Then $2,240 is your monthly housing cap. Stay under that and you sleep well. This is the heart of housing affordability. It’s also a key part of any mortgage affordability calculator Australia banks use behind the scenes.

The 36% Rule (Total Debt)

The second number. 36% of gross monthly income should cover all debts combined. That includes the home loan, car loan, credit card, HECS, and personal loans. So on $8,000 gross, total debt should not pass $2,880 a month.

This is your debt-to-income ratio Australia lenders watch. A good debt to income ratio for mortgage approval usually sits at or below this line. The rule is simple. The discipline is harder. Most folks slip on the second number.

Why the 28/36 Rule Matters for Borrowing in Australia

Banks don’t lend on vibes. They lend on ratios. The 28/36 rule sits inside their math models like flour sits inside bread. Skip it and you might still get a loan. Skip it for years and you’ll feel it.

Borrowing Capacity

Borrowing capacity Australia banks calculate is based on income, debts, and expenses. The 28/36 rule shapes the upper limit. Use any borrowing capacity calculator Australia offers and you’ll see the same logic.

Higher income? Higher cap. Bigger debts? Lower cap.

Borrowing Power

Borrowing power and capacity sound the same. They’re cousins, not twins.

Borrowing capacity is the math ceiling. Borrowing power is what the bank actually offers after stress tests. A borrowing power calculator Australia uses adds buffers. So your power is usually less than your capacity. Always. Try one before you make an offer.

Managing Debt Ratios

Knowing how to calculate debt to income ratio is gold. Add all monthly debts. Divide by gross monthly income. Multiply by 100.

Under 36%? You’re in the safe zone. Over 43%? Most banks frown.

Preventing Mortgage Stress

What is mortgage stress? It’s when housing eats more than 30% of your pre-tax income. You feel the pinch every payday.

The 28/36 rule sits below that line on purpose. It builds a moat. So one rate hike doesn’t drown you.

Mortgage Stress Benchmark

Mortgage stress Australia tracks closely. The classic benchmark is 30% of gross income on housing for low-to-moderate earners. Cross it and stress flags raise. Sydney mortgage stress is a real thing in many suburbs. Sydney housing affordability gets worse near the harbour and the inner west.

Serviceability Buffers

APRA tells banks to add a serviceability buffer when assessing loans. Right now it’s 3 percentage points above your actual rate. So if your rate is 6.2%, banks test you at 9.2%. This buffer is why borrowing capacity feels tight. It’s also why the 28/36 rule still works as a guide.

Budgeting for Buyers

A clean budget protects your future self. Use a moving house budget template before you sign. Pair it with a mortgage affordability Australia tool from MoneySmart. That combo answers the big question. How much mortgage can I afford Australia-wide without losing sleep?

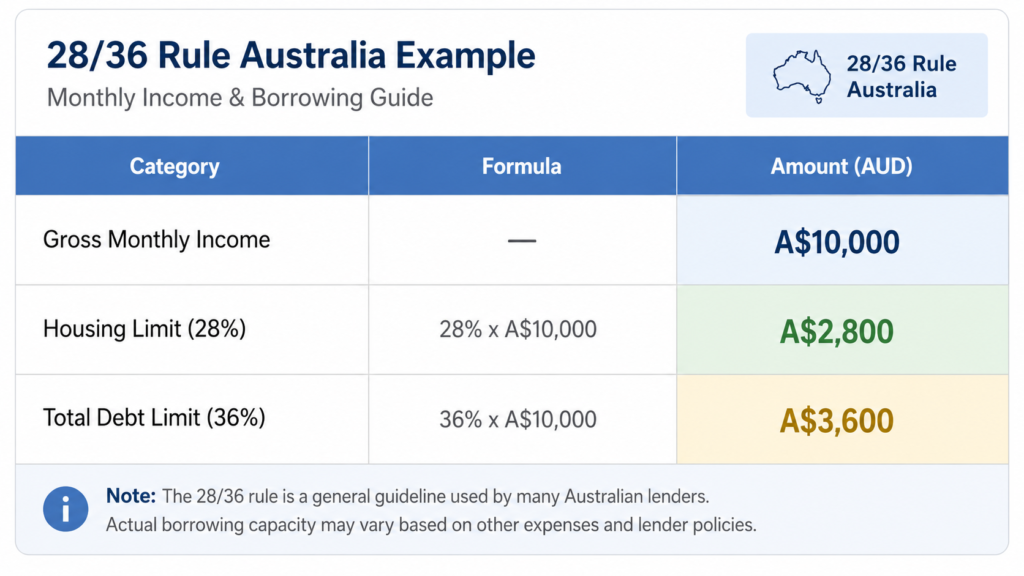

28/36 Rule Calculation Example

Let’s walk through a real-feel example. Numbers don’t lie. Spreadsheets don’t sugarcoat.

Gross Income of $10,000 per Month

Say your household earns $10,000 a month before tax. That’s $120,000 a year gross. Solid Sydney income. This is your starting line.

Max Housing Cost (28%)

28% of $10,000 equals $2,800. That’s your safe ceiling for the mortgage repayment, insurance, council rates, and strata. If your repayment alone hits $2,500, you’ve got $300 left for the extras. Things tighten fast.

Max Total Debt (36%)

36% of $10,000 equals $3,600. That’s your safe total monthly debt cap.

So $2,800 housing plus $800 for other debts. Maybe a car loan and one credit card. Anything more pushes you toward housing stress Australia families know too well. This is how to calculate housing affordability in 60 seconds. Faster than a flat white.

Other Names for the 28/36 Rule

People call it different things. The math stays the same.

Debt-to-Income (DTI) Ratio

DTI is the technical term. Banks lean on it daily. Debt to income ratio Australia lenders prefer sits at or below 6 times your gross yearly income for the loan itself. The 36% monthly figure works hand in hand with that.

Mortgage Stress Calculation

Some advisers call it a mortgage stress calculation. It flags risk before you sign. Used right, it answers the worry behind every first home buyer’s chest tightness.

Household Budget Capacity Rule

Older textbooks call it the household budget capacity rule. Same idea, fancier name. Whatever the label, the goal is the same. Keep housing under 28%. Keep total debts under 36%. Sleep at night. Smile by day.

Why Financial Planning Matters More Than Ever

Rates rise. Groceries climb. Energy bills sting. Sydney rents move like a tide.Planning isn’t a luxury anymore. It’s armor. A good plan covers four bases. Income. Debts. Savings buffer. Big future costs like moving or kids’ school fees.

The worst age to change schools Australia parents debate is between 12 and 15. Some say worst age to move a child is around mid-primary. So plan a move that respects the family rhythm too.

Moving away from family adds emotional weight. Plan for that. Phone calls. Visits. Time off work. All of it costs money. A solid plan turns chaos into a checklist. And a checklist beats anxiety every single time.

Why Lenders Use the 28/36 Rule When Assessing Mortgage Applications

Lenders aren’t villains. They run on risk math. The 28/36 rule lowers default risk. Lower default risk means more approved loans.

Here’s what lenders test. They test your income stability. They test your savings track record. They test your existing debts. They run a borrowing capacity calculator Australia accepts under APRA rules. The 28/36 rule gives them a clean benchmark. If you fit inside, your file moves faster. Lenders also stress test you against rate rises. They use that 3% buffer. Your real repayment might be $2,500 a month today. The bank tests you on $3,400. If the 28/36 rule still holds, you pass.

Banks worry about three big shocks. Job loss. Rate hikes. Surprise bills. The 28/36 rule cushions all three. Some banks use stricter caps. Others stretch a little. None of them ignore the math.

If you want a solid borrowing snapshot, run the numbers yourself first. Use a mortgage affordability calculator Australia trusts, like the MoneySmart tool. It’s free. It’s neutral.

What Happens if You Go Over the 28/36 Rule in Australia?

Push past 36% and the air gets thin.

You can still get approved. Many people do. But the cost of life goes up. The buffer goes down.

Here’s what tends to happen. You skip savings. You delay holidays. You feel every petrol price jump. Date nights turn into Netflix nights. Not the worst, but not the dream either. Then comes the real hit. A rate rise. Or a job change. Or a baby. Or a leaky roof. Suddenly the budget snaps. Going over the rule isn’t always wrong. Sometimes high earners with bonuses can stretch it. But for most Sydney buyers, this rule keeps the lights on.

Hidden costs of buying and moving at the same time add up fast. Stamp duty, legal fees, building inspections, lender mortgage insurance. Then come costs after buying a house. Pest control. Carpet steam clean. New blinds. Fence repair. Welcome to home ownership.

Is the 28/36 Rule an Official Lending Rule?

Short answer. No.

Long answer. Sort of.

It’s a guideline, not a law. But every serious lender uses some version of it.

Guideline vs lender tests

The 28/36 rule is a benchmark. Banks layer their own credit policy on top. So one bank may approve you while another says no. That’s why shopping around helps. A broker can show you who’s strict and who’s flexible.

Why 30% still matters

The 30% mortgage stress benchmark is older than the 28/36 rule in Aussie lingo. It still rules public discussion. Media uses it. Charities use it. Academics use it. Both rules point the same way. Don’t let housing eat half your pay.

How much of your income should go to mortgage? Aim for under 28%. Push to 30% only if you have a fat savings buffer.

What lenders assess

Banks look at five things. Income. Living expenses. Debts. Credit history. Deposit size. They run all five through a serviceability calculator. The 28/36 rule influences the output. It’s the silent boss in the room.

How much can I borrow home loan Australia banks ask. The answer comes from this exact mix.

How Sydney Housing Costs Change the 28/36 Rule

Now let’s get real. Sydney is its own beast. The classic 28/36 rule was built for average markets. Sydney is not an average market.

Greater Sydney snapshot

Median Sydney house prices have sat above $1.5 million in many suburbs. Apartments run cheaper but still strong. To buy at the median, you need a solid deposit. You need a strong income. And the 28/36 rule may demand a household income above $200,000 for a clean fit.

Sydney housing affordability is the toughest in the country for most buyers.

City of Sydney example

Take the City of Sydney council area. Apartments dominate. Strata fees add up. A $900,000 apartment with a 20% deposit means a $720,000 loan. Repayments at 6% over 30 years sit near $4,300 a month. Add strata, rates, and insurance. You’re past $4,800.

To stay inside the 28% cap, you’d need around $17,000 gross monthly. That’s $204,000 a year.See why so many Sydney buyers blow past the rule? It’s not laziness. It’s the market.

NSW transfer duty

Transfer duty is the new name for stamp duty in NSW. It’s a chunky one-off cost when you buy.

Use the transfer duty calculator NSW provides through Revenue NSW. Plug in the price. See the bill before you offer.

A $900,000 home triggers tens of thousands in duty. First home buyers may get exemptions or concessions under current thresholds.

This is one of the biggest hidden costs of buying a house in Sydney. Plan for it. Don’t be shocked by it.

Official tools to use

Want clarity? Use the official tools.

Try the ASIC MoneySmart mortgage calculator. Try the Revenue NSW transfer duty calculator. Try APRA’s published rules on serviceability buffers.

Free. Independent. No sales pitch.

What the 28/36 Rule Misses in Real Life

The rule is smart. It’s also blunt. It misses the messy human stuff. Real life isn’t a spreadsheet, mate. It doesn’t count childcare costs. Or private school fees. Or aged parents. Or a partner’s irregular contract income. Or HECS-HELP repayments creeping up.

It misses your moving day costs. How much do removalists charge? In Sydney, expect $150 to $220 an hour for two movers and a truck. The hourly rate for removalists rises in peak season. It misses the bond clean checklist Australia renters know by heart. It misses the change of address checklist Australia buyers should run on day one.

It misses lifestyle. Some folks happily live on rice and dreams to buy a place. Others won’t give up the gym, the brunch, the kids’ soccer fees. The 28/36 rule doesn’t judge. But it doesn’t ask either. It also misses one-off shocks. Surprise medical bills. A wedding. A funeral interstate. Life happens.

Treat the rule as the floor of common sense. Build your real budget on top.

How to Use the 28/36 Rule Safely

Right. So how do you actually use this thing?

Don’t bite off more than you can chew. That old Aussie line still hits hard. Start with your gross monthly income. Multiply by 0.28. That’s your housing target. Multiply by 0.36. That’s your total debt cap. Next, write down every cost. Mortgage. Rates. Insurance. Strata. Utilities. Internet. Phone. Subscriptions. Food. Petrol. Childcare. School fees.

Now use a moving house budget template if you’re about to move. Add removalist quotes. Add packing supplies. Add cleaning. Add the bond clean. Add change of address admin.

If your numbers fit inside 28/36, you’re rock solid. If they don’t, three options exist.

One. Buy a cheaper home. Boring but smart.

Two. Boost income. A side hustle, a salary jump, a partner returning to work.

Three. Cut debts before applying. Pay off the credit card. Sell the second car. Refinance.

How to avoid mortgage stress? Build a 3-month savings buffer. Keep insurance up to date. Avoid new debts in the year you buy.

What to do after buying a house? Update your address. Set up direct debits. Schedule a building inspection follow up. Build the emergency fund again.

Moving house checklist Australia buyers love includes utilities, mail redirect, school enrolments, and Medicare details. A change of address checklist Australia covers all of it.

Sydney Buyers and Movers, Six Brothers Has Your Back

Numbers tell one story. Moving day tells another. You can plan the perfect 28/36 budget. You can still feel wrecked if your move goes sideways.

That’s where Six Brothers Removalists steps in. We’re a local crew. Parramatta-based. Sydney-strong. We help you keep moving costs predictable. Predictable costs feed clean budgets. Clean budgets keep the 28/36 rule alive.

Need a quick van move for a studio or a two-bed unit? We’ve got that. Need an interstate run from Sydney to Brisbane or Melbourne? For a full walkthrough, see our ultimate guide to a stress free home move in Sydney.

Our team has handled thousands of Sydney moves. We know which streets are tight. We know which buildings need a lift booking. We know how to wrap a flat-pack like it’s a baby. Ring us on 1300 764 372. Or drop a line at info@sixbrothersremovalist.com.au. We’re at Suite 1 Level 5/58-60 Macquarie St, Parramatta NSW 2150.

So tell us. Are you ready to move with a budget that actually works? Or are you still guessing your borrowing power on a napkin?

The 28/36 rule won’t move your couch. We will.