Saving money in Sydney can feel like running uphill in thongs. Rent goes up. Groceries climb. Then moving day shows up with its own bill. So when a small, weirdly specific number like $27.39 starts trending on TikTok and finance blogs, people pay attention. And honestly? They should.

The $27.39 rule is dead simple. You save $27.39 every day. That hits $10,000 in a year. No spreadsheet wizardry. No fancy app. Just a steady drip of dollars into a savings account. It works because the number feels small. $27.39 is less than two coffees and a sandwich at a Parramatta café. But stack it for 365 days, and you have ten grand. Crazy how that adds up, right?

For families planning a shift across town or interstate, that $10K covers a lot. Bond. Removalists. New furniture. The hidden bits nobody warns you about. This guide breaks the rule down. We will cover the maths, the mindset, and how Sydney households can actually pull it off in 2026. Whether you are saving for a house deposit, an emergency fund, or your next move with six brothers removalists, this rule fits.

There is an old Aussie saying. “Save the pennies and the pounds look after themselves.” That is the $27.39 rule in nine words.

How the $27.39 Rule Works

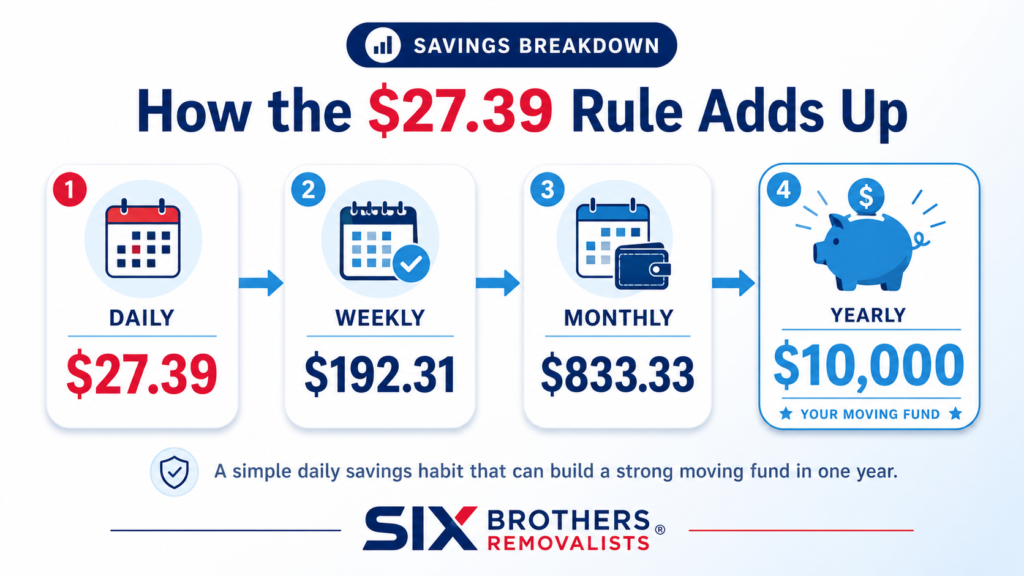

The rule sits on one bit of maths. $10,000 divided by 365 days equals roughly $27.39. That is your daily target.

You do not have to stash exactly $27.39 every single day. Most people batch it weekly or monthly. The number just gives you a clear daily benchmark to aim at. Think of it like a step counter for your wallet. You hit your daily steps, you stay healthy. You hit your daily $27.39, you stay rich-ish.

Daily: ~$27.40

Round it up to $27.40 a day if cents bug you. That is the easiest version. Some folks set a reminder on their phone and move the cash manually each morning. It works for people who like ritual. Coffee. Walk. Move $27.40. Repeat.

Weekly: ~$192.31

Most banks let you schedule weekly transfers. So the $192.31 weekly version is the most popular by far. Set it once. Forget it. Watch the balance grow. This works great if you get paid weekly or fortnightly. Match the transfer to payday and you barely notice the money leave.

Monthly: ~$833.33

The $833.33 monthly transfer is for the salary crowd. One transfer a month. Done. This version is psychologically harder. The lump feels bigger. But the maths lands the same: $10,000 a year, no drama.

Why the $27.39 Savings Rule Is Popular

Saving $10K sounds heavy. Saving $27.39 sounds like nothing. That gap is the whole magic. The rule went viral because it tricks the brain. Big goals feel scary. Tiny daily numbers feel doable. The $27.39 sits right in that sweet spot.

Actionability

You do not need a budget app. You do not need a finance degree. You just need a savings account and a transfer schedule. That low barrier matters. Most savings rules fail because they ask too much. This one asks for one decision, made once.

Habit Building

Daily money habits compound. Like brushing teeth, but for your bank balance. After three weeks, $27.39 feels normal. After three months, you check your savings and grin. The habit does the heavy lifting, not your willpower.

Automation

The real trick is automatic savings. Banks like ING, ubank, and Macquarie let you schedule transfers in seconds. Set it on payday. The money moves before you can spend it. That one setting saves more people more money than every budgeting app combined.

How to Use the $27.39 Rule to Save More Money

Most people start the rule wrong. They try to save $27.39 from leftover money at the end of the day. That never works. You flip it. Save first. Spend what is left. This is the golden rule of every savings system, including this one.

Here are the main ways Sydney savers actually pull it off in 2026.

Daily Savings

Move $27.39 every morning, before coffee. Use your bank app. It takes ten seconds. This works best if you like seeing progress fast. By Friday, you have nearly $200 stashed. That visible win keeps you going.

Weekly Adjustment

Pick a payday. Transfer $192.31 to a separate account. Done for the week. This is the version most Aussie families use. It pairs neatly with weekly groceries, weekly fuel, weekly wins.

Monthly Adjustment

If you are paid monthly, schedule $833.33 for the day after payday. Treat it like rent. Non-negotiable. The trick is timing. Move the money before you see it sitting in your everyday account.

Automatic Savings

A high yield savings account Australia wide is the best home for this cash. Banks like ubank and ING offer 5%-plus rates in 2026. Set the auto-transfer once. Walk away. Compound interest does the rest while you sleep.

Alternative Cadence

Some savers prefer a fortnightly savings plan. That works out to $384.62 every two weeks. This matches most Aussie pay cycles. Easy to align with your salary hitting the bank.

Funded by a Side Hustle

Drive Uber on Saturdays. Sell unused gear on Marketplace. Tutor for two hours after work. Whatever brings in the extra $27.39. This version is gold for renters in Sydney. Your salary covers life. Your hustle covers the savings goal.

Smaller Scale

Cannot do $27.39? Start at how to save $10 a day. That hits $3,650 a year. Still huge. The point is the habit, not the exact dollar figure. Saving $10 consistently beats saving $50 once a month.

Scalable Approach

When pay rises hit, scale up. Move from $27.39 to $35 or $50 a day. The system stays the same. Only the number changes. That is how regular people quietly build proper wealth.

How to Maximise the $27.39 Savings Rule

Saving the money is half the job. Making it grow is the other half. A bog-standard transaction account earns nothing. Your $10,000 sits there, slowly losing value to inflation. Lazy money is leaking money.

High-Yield Savings Accounts (HYSA)

Park the cash in a high yield savings account Australia offers, like ubank Save, ING Savings Maximiser, or Macquarie Savings.

In 2026, top rates sit around 5.10%. On $10,000, that is roughly $510 in free money every year. Tax applies, but still. Read the bonus interest rules. Most HYSAs need a monthly deposit and no withdrawals. Easy to meet if you stay disciplined.

Customization

The rule bends to fit you. Want to save for a $20,000 goal? Double it to $54.78 a day.

Want a softer pace? Drop to $13.70 a day for $5,000 a year. The framework holds either way.

Key Takeaways From the $27.39 Savings Rule

Before we go deeper, here are the bits worth remembering.

Total Saved

$27.39 a day equals $9,997.35 a year. Round to $10,000 for clean maths. That is real money. A new car deposit. A six-month emergency fund for most renters. A solid moving budget.

Psychology

Small numbers beat big numbers every time. $27.39 feels harmless. $10,000 feels heavy. Same money, different feeling. Use the brain hack. Do not fight it.

Best Practices

Automate the transfer. Use a separate account. Pick a high-interest one. Never touch it for everyday spending. That is the whole playbook. Four rules. Five minutes to set up. A year of quiet wins.

Does the $27.39 Savings Rule Work in Today’s Sydney Housing Market?

Sydney is brutal. Median house prices sit above $1.6 million in 2026. Rents in Parramatta hover around $750 a week for a two-bed unit. So can $10,000 a year really matter here? Short answer: yes. Long answer: it depends on what you save for.

For a house deposit, $10K alone will not get you to the front door. But it stacks fast over three or four years. Add government schemes like the First Home Guarantee, and the maths starts to work.

For renters planning a shift, $10,000 covers most moves easily. Bond, removalist costs, new furniture, redirected mail. Even an interstate run from Sydney to Brisbane fits inside that budget for many households.

This is where good planning meets good saving. Use the moving home calculator at sixbrothersremovalist.com.au to scope your real cost. Then aim your $27.39 rule at that number. There is no shame in starting small. The Sydney market punishes anyone who waits. So start today, even if today is messy.

Is the $27.39 Savings Rule Sustainable for Short-Term Aggressive Saving?

Here is the honest answer. The rule is built for the long haul, not a sprint.

If you need $20,000 in six months, $27.39 a day will not cut it. You will hit roughly $5,000 in that window. Decent, but short.

For aggressive saving, you stack rules. Use the $27.39 rule as your base. Add a no-spend month. Add round-ups. Add a side hustle.

A no spend month challenge can add $1,000 to $2,000 in pure savings. Round-up saving drips in another $20 to $50 a week. Stack those, and you accelerate fast.

The base rule keeps the habit alive while the boosters fill the bucket. That combo is the best way to save $10000 in under a year.

Practical Ways to Boost Your Savings in Sydney in 2026

Sydney living is dear. But there are real levers to pull. Let us look at the ones that actually move the needle.

Switch energy providers. A 15-minute compare on Energy Made Easy can save $400 a year for an average Sydney household.

Drop streaming services. Most homes pay for four or five they barely use. Cut two. Save $360 a year.

Bulk buy at Costco or Aldi. Households save 20-30% on groceries by switching the staples. That is easily $1,500 a year saved.

Refinance your mortgage. Even a 0.3% rate drop on a $700K loan saves $2,000 a year. Massive.

Use NSW rebates. The Energy Bill Relief Fund, Active Kids Voucher, and Toll Relief schemes all pay real money. Most Sydneysiders forget to claim them.

For families about to move, savings stretch even further. Smart packing, off-peak booking, and the right truck size all cut your final bill. Look at the how much do removalists cost breakdown on our blog before you book. The cheapest day, the right size truck, and a tight inventory list save hundreds.

Who the $27.39 Savings Rule Works Best For

This rule is not for everyone. Let us be real about who it suits.

Steady salary earners. If a fixed amount lands every fortnight, this rule is built for you.

Renters saving for a goal. A first home deposit. A wedding. A baby. A move from Sydney to Melbourne. The rule fits any clear, costed target.

Habit-driven savers. People who like systems and autopilot. If you hate decisions, set this once and forget it.

First-time movers. Anyone working through a first time moving out checklist needs a savings cushion. $10K covers bond, the truck, the new bed, the surprise costs.

Families with kids. School holidays, sports, growing feet. A buffer fund stops the panic mode.

The rule is less ideal for cash-only tradies, gig workers with wild income swings, or anyone deep in high-interest debt. Pay credit cards down first. Then start the $27.39 habit.

Australian Money Rules to Know Before Using the $27.39 Rule

Saving in Australia comes with rules. Knowing them keeps you out of trouble and helps you keep more.

Interest Is Taxable

Every dollar of interest you earn counts as income. The ATO sees it. So should you. Your bank reports interest to the ATO at year end. If you earn $510 on $10,000 in a HYSA, that goes on your tax return. Plan for it at tax time.

Deposit Protection

The Australian Government guarantees deposits up to $250,000 per person, per bank. Your $10,000 is safe. So is mine. So is your nan’s $80,000 sitting at NAB. This scheme, called the Financial Claims Scheme, kicks in if a bank fails.

NSW Cost-of-Living Support

NSW runs more rebates than most people use. Energy Bill Relief. Toll Relief. Active and Creative Kids Vouchers. School Fee Voucher. Seniors Energy Rebate. Check Service NSW every six months. New schemes drop. Old ones expand. Free money sits there waiting for the form.

When the $27.39 Savings Rule Falls Short

No rule is perfect. The $27.39 rule has real weak points. Let us name them.

It assumes stable income. If your pay is patchy, the rule wobbles. Casuals and freelancers may need a percentage rule instead.

It ignores debt. Carrying a credit card at 22% interest? Pay that first. Saving while debt grows is a leaky bucket.

It is slow. $10,000 in a year is tidy, not life-changing. Big goals need bigger inputs.

It does not account for inflation. $10,000 today buys less in five years. Your savings rate may need to rise yearly.

It can feel rigid. Some weeks, $27.39 a day is impossible. Sickness. Vet bills. Surprise fines. Life happens.

The fix is flexibility. Treat the rule as a guide, not a cage. Miss a week? Pick it up next week.

Better Ways to Adapt the $27.39 Rule

The base rule is a starting point. Here is how Aussie households tweak it.

Fortnightly Transfers

Most jobs in Australia pay fortnightly. So set a $384.62 fortnightly transfer, day-of-pay. Money moves before bills land. You barely notice it gone. By the end of the year, you are sitting on $10,000.

Separate Goal Account

Open a fresh savings account just for this rule. Name it. “Move Fund.” “House Deposit.” “Emergency.” Named accounts get raided less. Banks like ubank let you create up to ten goals. Use them.

Bill Cuts First

Before you start saving, audit your bills. Phone. Insurance. Streaming. Gym. Trim $50 a week from waste. That funds the rule by itself, no lifestyle pain needed.

Rebates and Vouchers

Stack every rebate you qualify for. Run the savings into the $27.39 fund. This is free-money fuel. Active Kids voucher? Goes in the fund. Toll relief refund? In the fund. Tax return? Half in the fund.

$27.39 Savings Rule vs Other Savings Challenges

So how does $27.39 stack against the other famous saving challenges? Let us compare.

52-Week Challenge

In the 52-week challenge, you save $1 in week one, $2 in week two, all the way to $52 in week 52. Total: $1,378. It is fun. It is gentle. But it saves way less than the $27.39 rule. Use it for kids’ pocket money goals, not house deposits.

Round-Up Saving

Apps like Raiz round every purchase up to the nearest dollar. Spare change goes to savings. Average Aussies save $700 to $1,200 a year this way. Pair it with the $27.39 rule and you stack two systems on autopilot.

No-Spend Month

You pick a month. You spend on nothing but essentials. Most households save $1,000 to $2,500. Brutal but effective. Run two no-spend months a year alongside the $27.39 rule. You will hit $13,000+ saved.

Fixed Weekly Plan

Same as our $192.31 weekly version. Predictable. Boring. Boring is good when it comes to money. The $27.39 rule beats most challenges on simplicity, output, and habit strength.

Best Savings Goals for the $27.39 Rule

What should you actually save for? Here are the four winners.

Emergency Fund

Three to six months of expenses. For Sydney renters, that is $15,000 to $30,000.

Run the rule for two years. You hit a solid emergency cushion. Job loss, vet bills, surprise medical costs. All handled. This is the emergency fund savings challenge version of the rule. The most useful one, by far.

Travel Savings

Saving for a Bali trip? Europe? A Queensland road trip with the kids?

$10,000 a year funds a serious holiday. Or two modest ones. Or a Japan ski week without the credit card hangover.

House Deposit Starter

$10,000 a year is the starter. After three years, you have $30,000 plus interest. Combine with the First Home Super Saver Scheme. Add a partner doing the same. Suddenly the deposit picture changes.

Annual Bills Buffer

Rates. Insurance. School fees. Car rego. These bills crush families when they land. Save $10K a year and use it to smooth annual bills. Pay yearly, get the discount, end the bill stress.

Tying the $27.39 Rule to Your Next Move

This is where the rule earns its keep for Sydney households. Moving is dear. Sydney moves especially so. The hidden costs of moving house catch people off guard. Bond on a new place. Connection fees. Mail redirection. Cleaning. Last-minute boxes. New curtains.

A standard local move in Sydney runs $1,200 to $4,500 for a two-bed unit. Interstate? $3,500 to $9,000+ for a three-bed home. Add storage and the bill grows again. Ten grand from the $27.39 rule covers most of this comfortably. Even better, it covers the surprises.

Use our how to reduce moving costs guide to plan smart. Pair it with the moving house budget template approach. Then book your removalist early to lock in the best rate. If the move is local, a speedy van move with two movers handles most studio to two-bed jobs. For bigger homes, a four to five-bed crew runs a different scale entirely.

The point is, the $27.39 rule turns moving from a credit-card panic into a paid-cash plan. That is a small revolution for most renters.

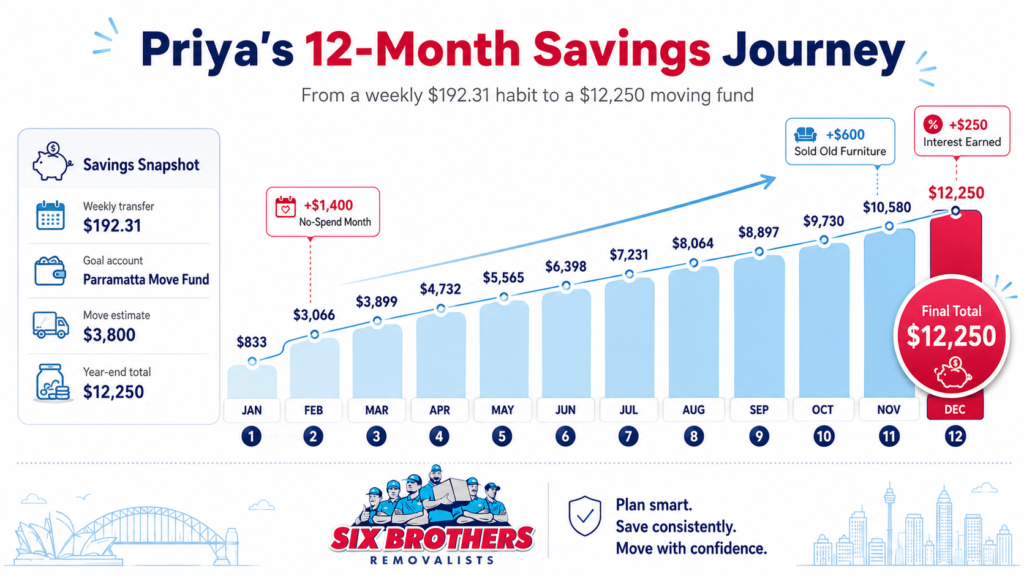

A Realistic 2026 Sydney Example

Let us run actual numbers. Meet Priya. She rents in Westmead. Earns $85,000 a year. Wants to move to a better place in Parramatta in 12 months.

Step 1. Priya opens a ubank Save account. Names it “Parramatta Move Fund.”

Step 2. She sets a $192.31 weekly transfer for every Friday.

Step 3. She uses the moving home calculator to scope her move. Result: $3,800 for a local two-bed shift with six brothers removalists.

Step 4. She runs a no spend month challenge in February. Adds $1,400 to the fund.

Step 5. She sells her old couch and bookshelf. $600 in. Earns 5% interest on the balance. Another $250 in.

Year-end total: $12,250. Move costs $3,800. She still has $8,450 left over for new furniture, bond, and a buffer.

That is the rule in action. No magic. Just a daily $27.39 habit and a clear goal.

Final Thoughts on the $27.39 Rule

The $27.39 rule is not the smartest savings system in the world. It is just the most doable.

It works because it asks little and delivers a lot. A coffee a day saves a house deposit starter, a holiday, or a stress-free move. That is a fair trade. If you are planning a shift across Sydney or interstate, give the rule a year. Stack it with smart booking, smart packing, and the right removalist. You will land in your new place with cash in the bank, not a credit card hangover.

So what is the $27.39 rule in one line? It is the daily promise that turns small change into life-changing money. Now go set up that transfer. Future-you is already saying thanks.

Need a Removalist Who Fits Your Saving Plan?

Six Brothers Removalists has helped Sydney families move smarter for years. Local jobs, interstate runs, full packing services. We move with care and quote with honesty.

Phone: 1300 764 372 Email: info@sixbrothersremovalist.com.au Address: Suite 1, Level 5, 58/60 Macquarie St, Parramatta NSW 2150

Get a free quote today. Book the move your $27.39 rule paid for.